General Mills (GIS) has recently issued its second quarter results for fiscal year 2014 missing consensus estimates in both the top and bottom lines. In this article I will analyze the company's recently reported historical results and its future outlook. Moreover, I will project its revenues and bottom line earnings to value the stock on the basis of these fundamentals to determine whether or not I would advise investors to invest or divest.

Brief Overview of Business Model

General Mills is one of America's most reputable companies. General Mills produces and markets consumer foods in domestic as well as international markets. The company purchases agricultural commodities from different vendors and processes these commodities to produce a wide array of products. Its sells both labeled and unlabeled products to commercial and noncommercial foodservice distributors, supermarkets, food chains, grocers and other distributors.

Future Expectations Regarding Commodity Prices

According to research conducted by OECD, global agricultural production is estimated to grow on an average of 1.5% per year during 2013-2022. During the past decade this growth was 2.3%.

The research highlights that the limited availability of agricultural land, increased production costs, production short falls and growing population are the main factors backing the trend. Hence, this supply demand mismatch will push prices up in the coming periods.

A Glance into the Company's History

As I mentioned at the beginning of this article, the company was unable to post alluring results during the second quarter of fiscal year 2014. During this period the company reported net sales of $4876 million almost flat year over year.

(click to enlarge)

Major contributors to flat sales were tumbling volume growth in the US, the negative impact of foreign currency translation and a decline in price realization and mix from convenience stores.

Moreover, the company generated net earnings of $550 million reflecting an increase of 2% year over year. This increase was driven by decreases in almost every category of expenses, partially offset by a higher tax rate and lower after-tax earnings contributed by joint ventures mainly because of the negative impact of foreign currency translation and flat top line sales.

Future outlook

In the developed world consumers have become health conscious and their preferences in terms of food seem to be shifting. Many consumers are now opting for organic, healthy and natural choices instead of the traditionally chemically infused fare.

People are shifting away from genetically modified foods and there is a lot of debate on the proposal regarding the labeling of genetically modified foods. This would drive up the prices of groceries and in such a case companies producing packaged food will take the hit. Moreover, an additional concern for the American packaged food industry is that the US Government seems to be weighing in on the matter. The state of Connecticut has already passed a bill requiring labeling on genetically modified foods and similar proposals are under consideration in other states of the country.

But in many high growth and emerging markets the demand for packaged goods is increasing and there are significant growth opportunities in China, India, Brazil and other such countries. General Mills is all set to the extract growth from these regions.

To counter the upcoming trends in the developed world General Mills entered the organic food market. Currently, the organic food segment of General Mills accounts for 32% of the entire revenues and has shown significant growth. However, the demand for packaged food, primarily in the US, will continue to see a decline.

Although the industry is very competitive, pricing pressure and increasing costs will certainly narrow the margins. However, I believe the organic segment will lead the company's growth in the developed world whereas processed and packaged food business of the company is expected to catch up growth in emerging markets.

Projections

In the table shown below, I have forecasted the revenues, net income as well as the margins of General mills till 2017. While forecasting the revenues I have accounted for the effect of declining sales of packaged food in the developed world, gradual increase in prices of products due to inflation and increased commodity cost's which could be passed on to the consumers. I have assumed an optimistic growth rate for General mills international operations, whereas while projecting the revenue contribution by convenience stores & food service segment I have been pessimistic due to the increased competition and other trends in purchasing pattern.

While, forecasting the net income I have assumed the cost of sales to increase at a rate of inflation plus the expected increase in commodity prices. I have assumed SG&A expenses and income contribution from joint venture to remain constant in terms of percentage of revenues.

(click to enlarge)

Valuation

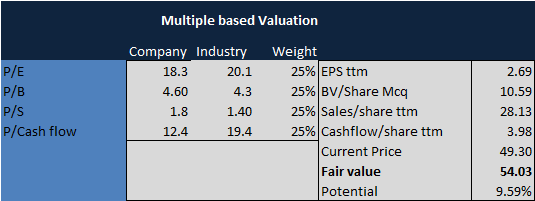

(click to enlarge)

The above table shows the fair value of General Mills derived through multiple based valuation approach. Earnings per share, Book Value, Sales and Cash flows have been calculated using company's trailing twelve month figures. Moreover, equal weights have been assigned to stock prices calculated by P/E, P/B, P/S, and P/CF ratios.

On the basis of given multiples of industry and the company fair value of the stock should be $54.03 representing an upside potential of 9.59%.

Conclusion

With increasing focus towards international expansion, brand development and shift towards organic food retailing in response to changing customer preferences, General Mills represents a very attractive investment opportunity in the consumer-defensive packaged food industry.

On the heels of sound financials, attractive valuation, reasonable returns, positive growth prospects and innovation capability General Mills deserves to be included in one's portfolio thus I would recommend the stock as a buy.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More...)

Business relationship disclosure: The article has been written by a Blackstone Equity Research research analyst. Blackstone Equity Research is not receiving compensation for it (other than from Seeking Alpha). Blackstone Equity Research has no business relationship with any company whose stock is mentioned in this article.

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire