Barron's stock picks for 2013 performed very well this year. In fact, at the time of the article, the average return for last year's stock picks was a whopping 38.5%, compared to a return on the S&P 500 of 28.6%. The stock picks for 2014 will be the 4th time Barron's published this list, but already, it is prefacing the predictions with a disclaimer:

It's unlikely that this bunch will do as well as the 10 stocks we selected a year ago

Perhaps that is a fair disclosure. We decided to perform our own evaluation of Barron's picks and include some of the off wall-street research recommendations. The following is our take on Barron's top picks:

American Airlines (AAL)

Investment Rationale

Airlines have been on a tear, and while we understand why Barron's would include the newly merged American and US Airways (LCC), we think it could be a speculative play on a pair of momentum stocks. The jury is still out on whether this merger will be financially successful, and while risks are high, so is the upside.

PM 101: Hold

Barrick Gold (ABX)

Investment Rationale

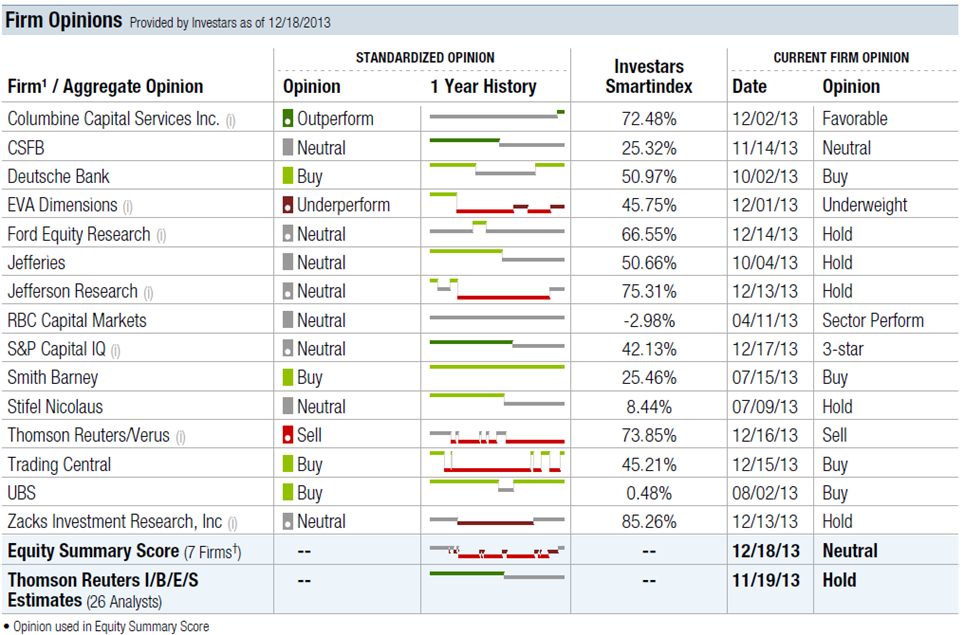

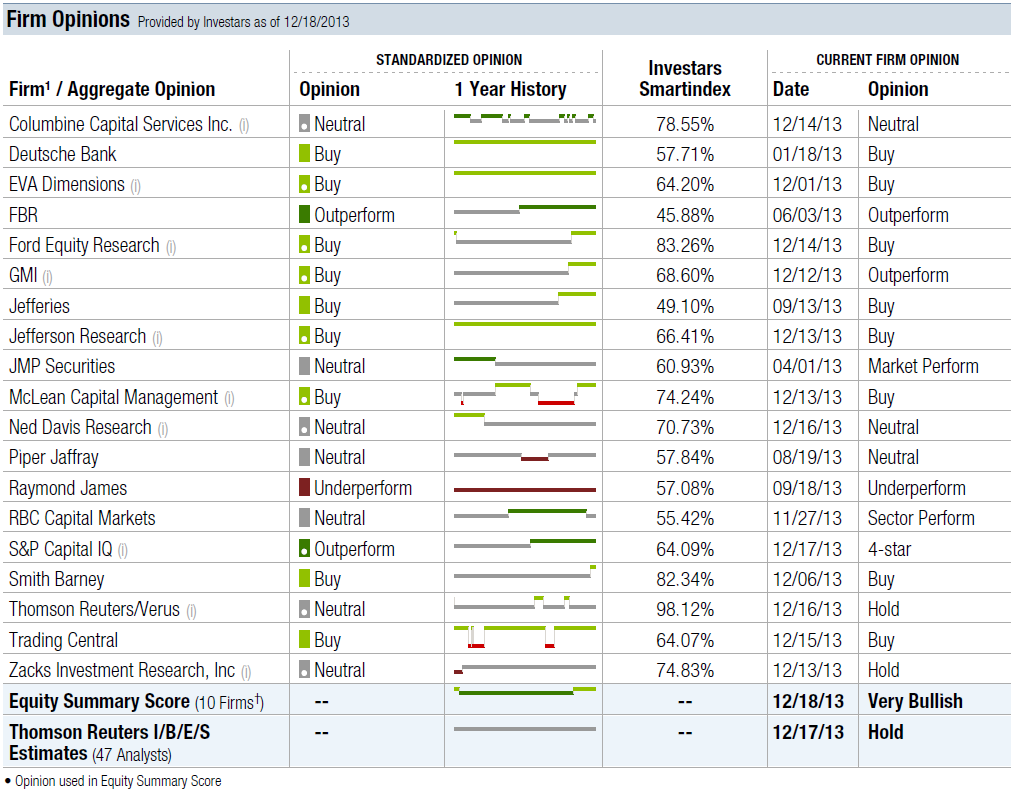

Gold took a beating in 2013 and so did the gold miners. Throughout 2013, we kept hearing about how the performance of gold miners relative to gold was at its widest in many years. Investors who followed that logic and invested in gold miners were severely punished for an investment rationale that we thought was quite sound. It just never materialized. 2014 may be just the year for that theme to play out, and apparently, Barron's thinks Barrick is the way to play it. Barrick is improving its cost structure, and new projects under construction should continue to drive costs down. One of the main risks is lower production due to suspended projects and inefficient mines that may take time to fix.

Firm opinions provided by Investars range widely, from outright sell to outright buy, with an average opinion of hold. See the chart below. Furthermore, Thomson Reuters estimates also rate it a hold. If it were us, we would wait to see some turnaround in Gold before jumping in to this one.

PM101: Hold

(click to enlarge)

Canadian Natural Resources (CNQ)

Investment Rationale

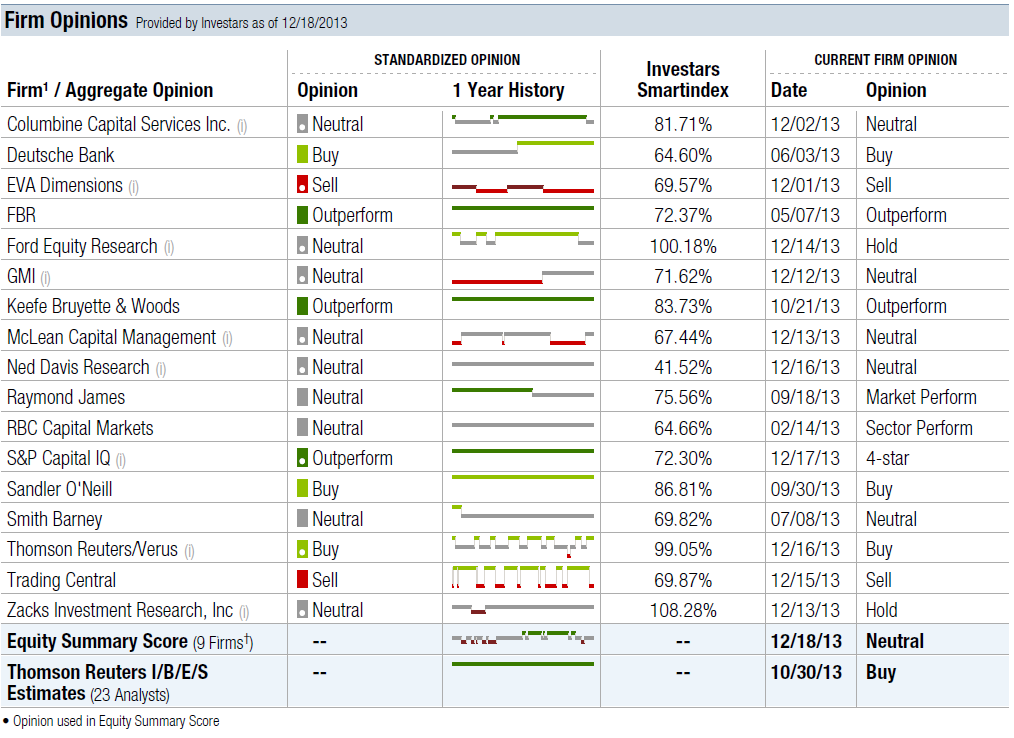

North America is experiencing an oil and gas boom. Some experts have gone as far as stating that the US will become a net exporter of oil in the near future. Well, CNQ is not in the US, but just North of us, and it is gaining access to the Gulf Coast market. Its multiyear plan is set to increase production beyond the next few years. Its biggest challenge is the shift into higher quality production and geographic expansion. Despite that, we like this E&P player!

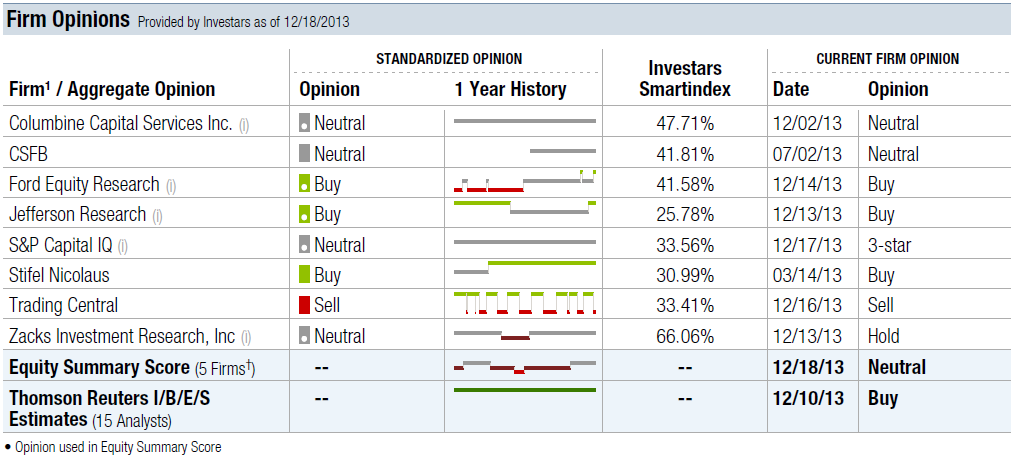

While non wall-street opinions are few, we found only one sell, and it came from Trading Central, which has a tendency to change its recommendation frequently. See 1 year history in chart below.

PM101: Buy

(click to enlarge)

Citigroup (C)

Investment Rationale

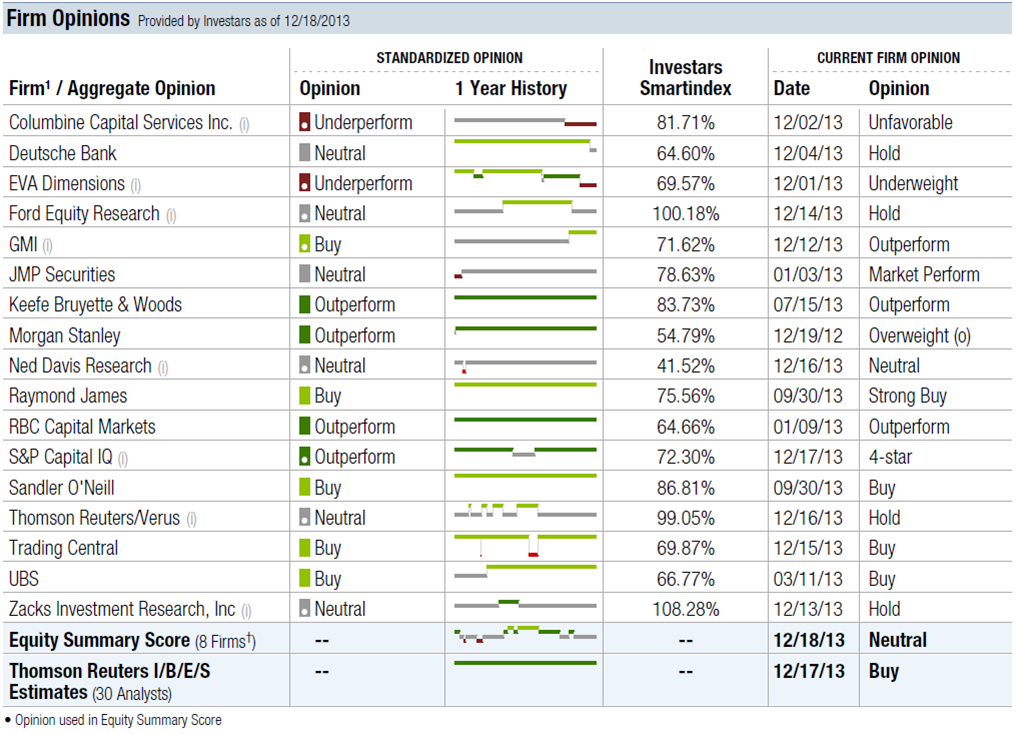

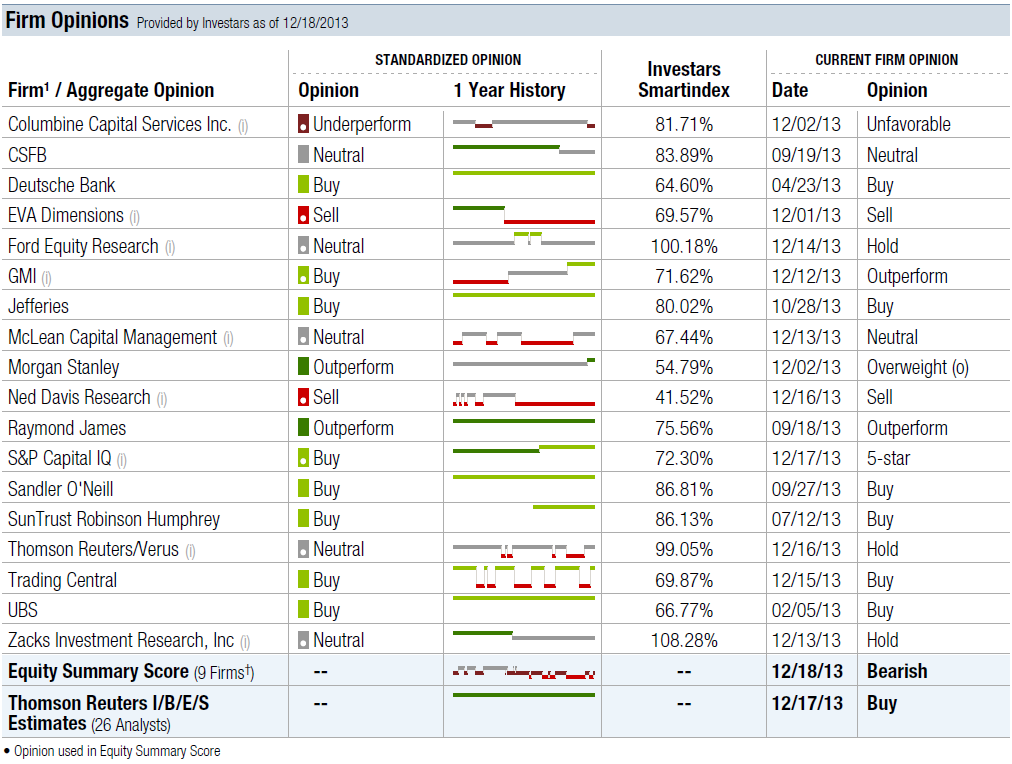

Citigroup is a global conglomerate with meaningful exposure to emerging markets which should continue to drive banking business while US and European consumers and businesses remain cautious. Citi's biggest challenge is the continued focus on changing the culture embedded in the company during and after the government bailout. We are strongly considering an investment in Citi and agree with the Thomson Consensus rating below. Outside Wall Street, there also seems to be a positive view of the stock, but with a moderate number of neutral opinions.

PM101: Buy

(click to enlarge)

Deere & Co.(DE)

Investment Rationale

It occurred in developed markets over many years, why shouldn't it occur in emerging markets also? We are referring to the consolidation of farm land in many countries, as large farms buy smaller farms to achieve economies of scale or in some cases, because the small farmer just isn't profitable anymore. Larger farms translate into a greater need for farming equipment, and hence the positive prospects for Deere.

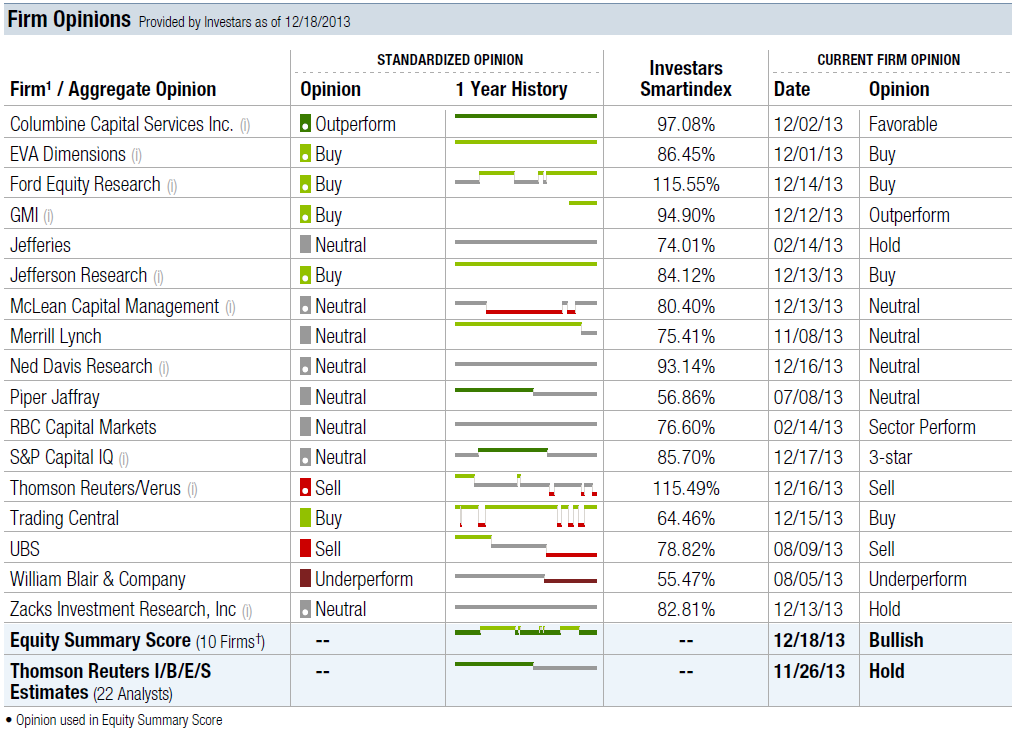

Interestingly, Wall Street seems to be lukewarm towards Deere, while the independent analysts are bullish. See chart below.

We would tend to agree with the latter, but we are also mindful of the risks of an economic slowdown in Europe or North America that could have negative consequences. Nevertheless, we think the risks of a slowdown are muted and that we may actually see emerging markets turn around sooner than the consensus is predicting.

PM101: Buy

(click to enlarge)

General Motors (GM)

Investment Rationale

GM needed some help from the US government to survive, and it sure seems it has taken full advantage of its second chance. Labor costs, historically high across all US automakers, have been reduced from $16 billion in 2005 to about $5 billion today. Furthermore, GM is actually making nicer cars in the higher price ranges, which have higher margins.

The biggest challenges it faces are twofold in our opinion: on the one hand, it has to convince Americans to buy American, which has not been the trend, at least not on the coasts. Many people in our offices drive German cars, and the rise of other foreign carmakers poses an additional challenge. I mean, have you seen the new Hyundais and Kias? Both Korean manufacturers have come a long way.

It seems that most analysts agree with Barron's and so do we. We think it has more to do with the level of operational safety cushion it has in the event of recessionary type sales numbers. By some estimates, GM's breakeven is about 10 million vehicles. The US would have to be in a recession for GM unit sales to be so low. We don't see that happening any time soon.

PM 101:Buy

(click to enlarge)

Intel (INTC)

Investment Rationale

We really struggled with this one. We like the semiconductor space, and Intel has been a leader in the industry since, well, as far as we can remember, really. It probably has the deepest pockets of cash of any semiconductor company, and it will continue to be a leader in cutting-edge technology. The stock will do very well. The reason for our hesitancy is only because our favorite stock is Qualcomm (QCOM), which also happens to be in the semiconductor industry. We will take the easy road here and suggest an investment in both companies, but if we could only choose one, we would go with Qualcomm.

PM 101: Hold

(click to enlarge)

Met Life (MET)

Investment Rationale

The growth opportunity for Met Life is in Asia, through its recent acquisition of Alico. It also has a very stable business in the group life insurance for corporate customers. It is still registered as a bank holding company, but if it receives approval to deregister, it's quite possible Met can instill a variety of new shareholder friendly policies. We are not convinced of its ability to manage its portfolio of increasingly risky securities (i.e. mortgages) nor do we like its prospects in an environment with little to no inflation. Longer term, yes, but 2014 may be too early for MET.

PM 101:Hold

(click to enlarge)

Nestle (OTCPK:NSRGY)

Investment Rationale

Do you like chocolate? Do your spouses like chocolate? Do you drink bottled water? Do you have a dog? Cat? Baby? If you answered yes to any of these, then you probably buy something from Nestle. Nestle is a global conglomerate that dwarfs the likes of Kraft (KFT), General Mills (GIS), and Danone (OTCQX:DANOY).

It may be too reliant on emerging markets to generate growth, and any drop in spending in the developed regions of the world could hurt sales, but this is the type of company that should be included in any investor's core holdings. Will it 'outperform' in 2014? That is a tough question, and we will skirt around it by stating that yes, it should be part of an investor's portfolio, but it shouldn't be thought of as providing growth of capital. Nestle is a steady-as-she-goes type company. Until 2012, revenues hadn't grown more than single digits since at least 2003, if not longer. (We only had data to 2003)

Unfortunately, we couldn't find the Investars chart for Nestle, but Wall Street estimates are for flat earnings growth in 2014 (In CHF, currency movements may have an effect as well in USD terms)

PM 101: Hold

Simon Property Group (SPG)

Investment Rationale

Oh, the REITs! Everything we read is negative on REITs. The reason for the negative outlooks is that REITs are considered an income play. We could argue back and forth on this all day and we are of the thought that REITs are not as sensitive to interest rate changes as traditional fixed income. But like the baby in the bath water, REITs tend to get lumped in with bonds when interest rates rise. We saw it this summer, and we continue to read about the dim prospects for REITs. We like the senior housing REITs, for example, including Senior Housing Trust (SNH) and Ventas (VTR) (Read SNH Article and VTR Article), and we are somewhat relieved to see Simon included on this list. There are also other types of REITs that are attractive in certain economic environments, such as those we mention in REITs for a Rising Rate Regime. The chart below is more consistent with what you might read elsewhere about REITs, but Simon is in a good space.

Simon is the largest owner of shopping malls in the US, and consumer confidence is at 'feel good' levels. Typically, when the consumer feels good, they shop, and Simon will be the beneficiary of that. We also keep seeing improvements in the labor market, albeit slowly. This too will impact consumer confidence in the form of higher disposable income, a portion of which will end up being spent at a Simon mall.

PM101: Buy

(click to enlarge)

Looking forward to 2014

Keep in mind that it is very difficult to predict or forecast the movements of equity investments, and in particular, over a specific period of time, and one that is not very long. Barron's has now done this for the fourth consecutive year, and while last year was a stellar year for their picks, there is no guarantee that this year's picks will be as successful. The same holds true for our opinions as well.

Take these predictions with a grain of salt and understand that while they may not pan out in 2014, each one of these companies should perform well over a longer period of time. Until next year…good luck and happy holidays.

Disclosure: I am long QCOM, SNH, VTR. I am considering positions in GM and C. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire