Shares of Athens, Greece-based DryShips (DRYS), that is a global shipping company specializing in carrying drybulk commodities and petroleum and petroleum-related cargoes, have rallied strongly recently, rising 27% in just the last week, and have almost tripled from their $1.65 low earlier in June this year. The rebound in DryShips shares is almost in tandem with the rise in the Baltic Dry Index (BDI) that has also almost tripled from its lows earlier this year (see Chart), and among many of its drybulk shipping peers, including, (I) Athens, Greece-based drybulk commodities shipper FreeSeas Inc. (FREE), up almost three-fold in the last three weeks; (ii) Piraeus, Greece-based drybulk shipping and logistics company Navios Maritime Holdings Inc. (NM), that is up more than three-fold from its lows last year; (III) Eagle Bulk Shipping Inc. (EGLE), the largest U.S. based owner of handymax drybulk vessels, that is up more than three-fold from its lows last year; and (iv) Palaio Faliro, Greece-based drybulk shipping services provider Diana Shipping Inc. (DSX), that has more than doubled off of the lows from last year.

(click to enlarge)

The BDI is issued daily by the London-based Baltic Exchange, based on daily submissions from a representative panel of international shipbrokers. It provides an assessment of the price of moving the major drybulk raw materials such as coal, metallic ores, building materials and grains, along 23 global shipping routes measured on a time-charter basis. Besides the BDI, that is the most popular measure with investors, the Baltic Exchange also issues separate indices for each class of vessels, namely for Capesize, Panamax, Supramax and Handysize vessels, and the BDI is actually a weighted average of these individual indices.

As powerful as the rally off of the lows from mid-2013 looks on the one-year chart for BDI above, it is actually just a blip when put in the context of BDI's long-term performance. The index peaked in May 2008, at 11,793 points, and then fell about 94% in the ensuing six months as the global recession took hold, bottoming out at a low of 663 points. The BDI is a very volatile index, as while demand for shipping rises and falls incrementally, the supply of ships is inelastic, as it takes about two years to build a new ship, and once built they are too expensive to take out of circulation. Thus, even marginal increases or decreases in demand can cause shipping rates and hence the BDI to move by larger amounts. The current rally still puts the BDI at about 80% below the highs set prior to the global recession, giving it ample room to the upside as the nascent global recovery takes hold.

Drybulk shipping remains a backbone of international trading, and with the global recovery, drybulk sector shipping rates may continue to rise going forward. Demand is up, as reported in the company's latest 3Q/2013 presentation, with exports by Brazil & Australia, the two largest iron ore exporters in the world, up 15.8% year-over-year. Also, iron ore imports by China, that buys the majority of seaborne iron ore cargoes, are up 16.9% year-over-year, and Chinese coal imports are also up 21.4% year-over-year. Meanwhile, drybulk fleet growth is normalizing (see Chart), as Capesize and Panamax deliveries fell off significantly in 2013 and are projected to fall off even more next year, while demolitions rose until last year and are projected to flat-line in 2014.

Dryships also has a strong exposure to the spot market, with 20 out of its 28 Panamax vessels, its two Supramax vessels, and one out of its 12 Capesize vessels operating on a spot basis, which should aid earnings going forward if the BDI continues to climb upward as international drybulk trade demand growth seems to indicate. The company has estimated that if spot rates rise by $5,000, it will add $65.8 mill. & $79.3 mill. to its EBITDA or free cash flow generation, and the numbers rise even higher to $131.6 mill. & $158.7 mill. respectively if spot rates rise by $10,000, and to $263.2 mill. & $317.3 mill. if spot rates rise by $20,000.

In the latest 3Q/2013, DryShips reported a loss of 7 cents per share, missing estimates by 2 cents, and revenues came in at $404.9 mill., up 18% year-over-year and squarely beating analyst estimates of $354.7 mill. Going forward, analysts are projecting that revenue and earnings will rise from $1.41 bill. & $0.28 loss projected for FY 2013 to $2.03 bill. & $0.27 in earnings for FY 2014, and rise further to $2.41 bill. & $0.59 in earnings for FY 2015. Thus, at Friday's closing price of $4.68, DryShips shares trade at an attractive 17x FY 2014 and 8x FY 2015 earnings. Also, based on the current $487.4 mill. in EBITDA on a trailing twelve month (TTM) basis, its shares trades at a 13.1 EV/ EBITDA ratio. In comparison, among its drybulk shipping peers, FreeSeas currently has a negative EBITDA and losses, Eagle Bulk Shipping is projected to incur losses in FY 2015 and trades at 20x EV/EBITDA, Diana Shipping is trading at 27x the FY 2015 earnings estimate and at 17x current EBITDA, and Navios Maritime shares trade at 16x FY 2015 earnings and at 35x EV/EBITDA. Also, with the exception of Navios Maritime, that offers a 2.4% dividend yield, none of the others, including DryShips, currently offers a dividend.

DryShips has a high debt overhang of $5.3 bill., with only $506 mill. in cash and cash equivalents, which continues to weigh down on the shares, especially keeping in mind the tough conditions that the shipping industry has gone through in the last few years, with several major players having to declare bankruptcy. DryShips survived the tumultuous times by diluting shareholders, with its shares outstanding having gone up from 36 mill. shares in 2007 to 211 mill. shares in 2009, and 376 mill. shares in 2011. However, that pace has slowed down quite a bit as the company is ending 2013 with shares outstanding at 383 mill. shares, only 2% higher from the levels two years ago.

The decision by the company earlier this month to suspend their previously announced program of at-the-market offering to raise up to $200 mill. is positive in that context as it indicates that DryShips' current cash reserves may be sufficient for the time being to finance operations, and no further dilution is needed at least for the time being. Furthermore, it may also be interpreted that DryShips management is confident in the turnaround and that its practice of frequently going to the capital markets to raise cash to finance operations could be nearing an end.

DryShips also is no longer just a drybulk shipper, it also has ten oil tankers, and by virtue of its majority ownership of offshore deepwater drilling services provider Ocean Rig UDW Inc. (ORIG), it also owns six ultra-deepwater semi-submersible drilling rigs and four ultra-deepwater newbuilding drillships. Its ownership of ORIG is particularly positive as ORIG has been reporting strong profits, at $0.30 per share or $39 mill. in the latest 3Q/2013, and is projected to report $1.86 per share or $245 mill. in FY 2014, and $2.67 per share or $352 mill. in FY 2015. Backing out those numbers from the analyst earnings estimates for DryShips, it seems that current analyst estimates are for losses to continue into FY 2014 and FY 2015 from DryShips core drybulk shipping business. If rates turnaround as we suspect, then there may be even more upside to these analyst estimates, making DryShips shares a buy despite the recent strong run-up. However, we would wait for shares to pull back down and consolidate in the $4 to $4.50 range before making any purchases, so as to minimize the short-term downside risk.

Guru and Mega Fund Managers Are Bullish on DRYS

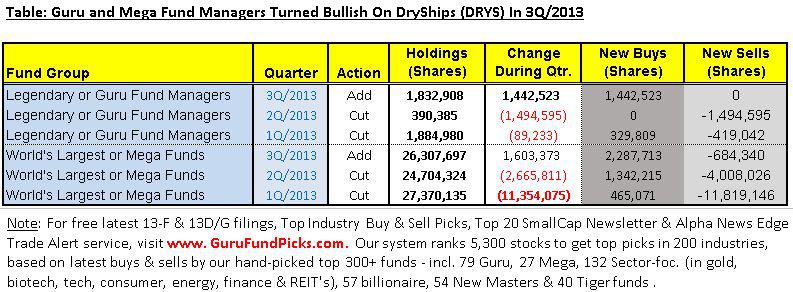

Leading fund managers, including our 79 legendary or guru fund managers, and 27 of the world's largest or mega funds, turned bullish on DryShips in 3Q/2013, after selling shares in the prior two quarters. Mega funds reduced their holdings from 48.2 mill. shares at the end of 3Q/2012 to 26.3 mill. shares at the end of 2Q/2013, selling 45% of their holdings in the company over three quarters, before adding back a minor 1.60 mill. shares in 3Q/2013. Guru fund managers too reduced their holdings in DryShips from 3.2 mill. shares at the end of the 3Q/2012 to 0.4 mill. shares at the end of 2Q/2013, before adding back 1.4 mill. shares in the latest 3Q/2013.

We have been following the activities of leading fund managers via numerous articles on Seeking Alpha, and on our website GuruFundPicks.com, and have observed a strong correlation between the activities of leading fund managers and the price performance of stocks in the succeeding quarters. Hence, we view the small accumulation of DryShips shares by leading fund managers in the latest 3Q/2013 as a positive, lending further credence to our thesis that DryShips shares are in buy territory based on the projected turnaround in the BDI index and the promising prospects for its majority owned subsidiary ORIG.

The top guru fund buyers of DryShips during the latest 3Q/2013 were Chicago-based mutual fund company Driehaus Capital Management (click on the links to view their full summarized 13-F filings), that bought a new 0.83 mill. share position, and global macro hedge fund manager Soros Fund Management, that bought a new 0.59 mill. share position. Among mega funds, the top buyers was mutual fund manager Fidelity Investments, that added 1.93 mill. shares to its 6.68 mill. share prior quarter position, and the top holder was Deutsche Bank, with 15.20 mill. shares.

(click to enlarge)

Disclosure: I have no positions in any stocks mentioned, but may initiate a long position in DRYS over the next 72 hours. (More...)

Business relationship disclosure: Business Relationship Disclosure: The article has been written by the Hedge and Mutual Fund Analyst at GuruFundPicks.com. GuruFundPicks.com is not receiving compensation for it (other than from Seeking Alpha). GuruFundPicks.com has no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Additional Disclosure: Use of GuruFundPicks’ research is at your own risk. You should do your own research and due diligence before making any investment decision with respect to securities covered herein. You should assume that as of the publication date of any report or letter, GuruFundPicks, LLC, has a position in all stocks (and/or options of the stock) covered herein that is consistent with the position set forth in our research report. Following publication of any report or letter, GuruFundPicks intends to continue transacting in the securities covered herein, and we may be long, short, or neutral at any time hereafter regardless of our initial recommendation. To the best of our knowledge and belief, all information contained herein is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable, and not from company or persons who have a relationship with company insiders.

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire