Costco Corp. (COST) operates a productive retail stores base and has been making efforts to expand its store base in the U.S. and international markets. COST's growth story remains attractive and the company has been delivering healthy results, which are driven by store expansion and growth in membership fees. Also, the company continues to hold a dominant position in the industry and its strategy of offering products at heavy discounts has portended well for the company's performance and the stock price despite the recent sluggish economic conditions. Moreover, current valuations remain attractive for the stock, as the company is currently trading at a forward P/E of 21x as compared to its own three-years average historical P/E of 23x.

Financial Performance 1Q FY2014

The company has been delivering a healthy financial performance in recent times, despite a tough consumer spending environment. Recently, the company reported total revenues of $25 billion for 1Q FY2014, up 5.5% as compared to the corresponding period last year. Total revenues for the quarter were positively affected by a 4.5% increase in traffic. Also, COST's comparable same stores sales increased by 3% in the quarter, representing a 3% and 1% increase of same stores sales in the U.S. and international markets, respectively. Its membership revenue for the quarter remained strong, as it increased by 38 million year-on-year, driven by new memberships and fee increases.

COST reported earnings per share of $0.96, up 1.1% as compared to the same quarter last year, missing consensus estimates of $1.02. The company's performance for the quarter was adversely affected by foreign currency movements and lower gas prices. As the company has been making efforts to expand its international operations, foreign currency remains a risk to its top and bottom line results.

Store Expansion

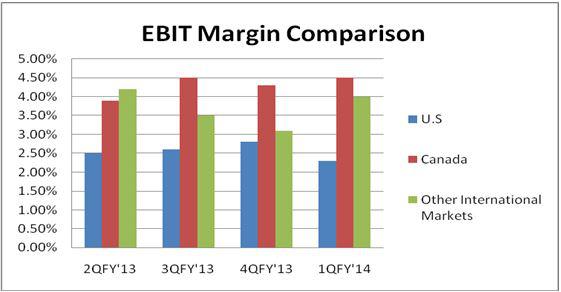

The company has been making efforts to expand its stores in the U.S. and international markets, which remains an important stock price driver. Focus of the stores expansion has been primarily on international markets, which offer higher margins and have a less competitive industry environment in comparison to the U.S. The following table shows EBIT margin comparison between the company's U.S., Canada and international markets segments.

(click to enlarge)

Source: Company Reports and Calculations

International stores expansion opportunities remain attractive and profitable for COST as compared to expanding stores in the U.S., given that the former offers a less competitive industry environment, higher margins and lower costs.

In the near future, the company expects that 60% of its new store openings will be in international markets, targeting mainly Asian and Australian markets. In the ongoing year, FY2014, the company expects to open 16 new stores in the U.S., four in Australia, three in Canada, one in Mexico and two each in Japan, Korea and Spain. Also, the company has plans to penetrate France by fiscal year 2015. The company currently has 648 total operational stores, including 461 in the U.S., 87 in Canada and 100 in the rest of the international markets.

The company has been taking measures to expand its footprint in international markets, and has been developing systems and incurring capital expenditures, which in the short term might adversely affect the company's bottom line results; however, in the long term, the expansion efforts will fuel earnings for the company.

E-commerce

The wholesale and retail industry, to a certain extent, is exposed to increasing popularity of e-commerce business transactions. The company does have a limited online presence, as it generates approximately 2.5% of its total sales online. In the last two years, COST has made efforts, to some extent, to strengthen and grow its online presence by redesigning its site, launching a mobile application and initiating its e-commerce operation in Mexico in the last quarter. These efforts have brought notable results, as e-commerce sales increased by 24% in the last quarter, as compared to the corresponding period last year. I believe COST needs to further ramp up its efforts to expand its online presence to keep up with the changing industry environment, which will help it grow and strengthen its market share. The company's competitor, Target Corp. (TGT), has undertaken three acquisitions in the ongoing year to increase its online presence.

Share Repurchases and Dividend

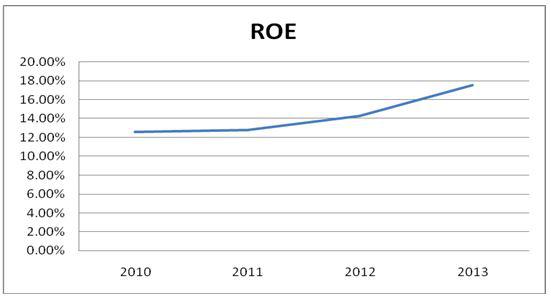

The company has a shareholder-friendly management, which has been sharing its success with shareholders via share repurchases and dividends. Since 2010, the company has repurchased $1.90 billion worth of common stocks, representing almost 4% of the current market capitalization of $51.5 billion. COST generates significant free cash flows and I believe the company will continue to undertake share repurchases aggressively, which will magnify its ROE in the future. The company's ROE increased from 12.5% in 2010 to 17.6% in 2013, as shown below.

(click to enlarge)

Source: morningstar.com

Other than aggressive share repurchases, the company offers a safe dividend yield of 1.10%, backed by its solid free cash flows. The following graph shows the healthy relationship between COST's annual dividend and free cash flows.

(click to enlarge)

Source: Company Reports and Calculations

Conclusion

COST is among the leading companies in the industry. The company is well positioned to improve its same store sales and strengthen its market share. Also, COST's efforts to expand its operations in the U.S. and international markets are key future earnings growth drivers, and will help the company improve its margins as international markets have better margins as compared to domestic markets. Consistent with the company's expansion plans, analysts have projected a robust growth rate of 12% per annum for the next five years.

Moreover, current valuations seem to be attractive for the company. The stock is currently trading at a cheap forward P/E of 21x, in comparison to COST's historical three years average P/E of 23x. Also, the stock offers potential price appreciation of 9%, based on my price target of $127. The price target of $127 was calculated using the historical three years average P/E of 23x and next year's (FY 2015) EPS estimate of $5.50.

Average P/E | EPS estimate | Price Target |

23x | $5.5 | $127 |

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire