ConAgra Foods (CAG) released its 2014Q2 earnings report before market open on December 19 and, later that morning, held the corresponding conference call. The stock traded up on heavy volume (~3x average) to close at $33.47 for a 5.28% gain on the day. However, the rally still only left the stock with an 11.5% year-to-date gain, which is less than half of the S&P 500 YTD gain. In this article, I'll touch on the main takeaways from the earnings report and conference call, as well as offer both general information about the company and my opinions of the investment case.

(click to enlarge)

Company Overview

ConAgra Foods is one of North America's largest packaged food companies, the largest private-brand packaged food business in North America and a strong commercial and foodservice business. ConAgra's consumer portfolio includes brands found in 97% of America's households such as Blue Bonnet, Chef Boyardee, DAVID Sunflower Seeds, Swiss Miss, VanCamp's, Healthy Choice, Hebrew National, Manwich, Marie Callender's, Slim Jim, LaChoy, Orville Redenbacher's, Peter Pan Peanut Butter, Parkay, P.F. Chang's Home Menu, Wesson Oils and many others; along with food sold by ConAgra under private-brand labels in grocery, convenience, mass merchandise and club stores. ConAgra also has a strong commercial foods presence supplying various well-known restaurants, foodservice operators and commercial customers in 120 countries with frozen potato products through its Lamb Weston subsidiary. In addition, ConAgra supplies a wide variety of other food products and ingredients through subsidiaries such as Spicetec and JM Swank, which also offers a range of logistics services. ConAgra also owns 44% of Ardent Mills, a joint venture that will combine ConAgra Mills' flour-mill operations with those of Cargill and CHS (CHSCP). ConAgra also operates Child Hunger Ends Here.com for its twenty-year commitment to fighting child hunger in America. The 2013 campaign resulted in ConAgra donating the monetary equivalent of more than three million meals to Feeding America, the nation's largest domestic hunger-relief organization. For more about ConAgra, see the corporate website.

ConAgra also operates the following websites:

Hungry To Help -- ConAgra Foods Foundation blog

ConAgra Science Institute -- nutrition resources for health professionals

ReadySetEat -- interactive recipe ideas

Earnings Review

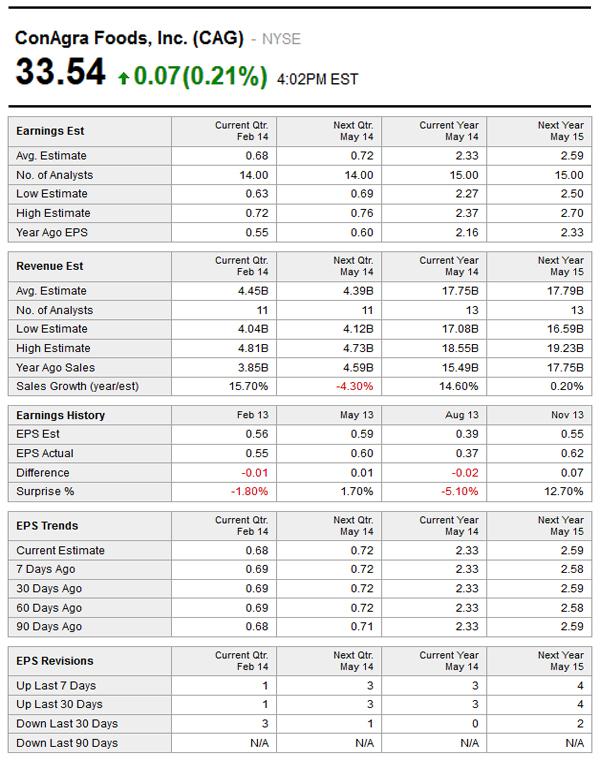

CAG reported 2014Q2 revenue of $4.71 billion, exceeding the consensus estimate of $4.63 billion. Revenue increased by more than 26% over the prior-year period and 12% over the previous quarter. For the current quarter (Q3), the consensus revenue estimate at this time is $4.40 billion.

CAG reported 2014Q2 adjusted EPS of $0.62 per share, beating the $0.56 consensus estimate by ~12%. The $0.62 EPS represents a ~9% increase over the prior-year period and drastically exceeds the disappointing $0.37 of Q1. Some earnings initially expected in Q1 were not fully realized until Q2, resulting in the unusually low Q1 EPS and boosting Q2. At the same time, I don't believe the Q2 boost was equivalent to the Q1 miss since EPS likely would have increased even more by Q2 if the pace of growth was as fast and steady as originally anticipated. In other words, as I will discuss further below, I think original expectations were overzealous. For the current quarter (Q3), the consensus estimate at this time is $0.67.

Each segment performed well, but I think it is still too early to evaluate them individually after recent restructurings. As to be expected following any large acquisition, CAG implemented organizational changes during the quarter that resulted in new reporting segments. The new segments are: Consumer Foods, Commercial Foods and Private Brands. The segments are discussed in detail in the earnings call. As CEO Gary Rodkin explains in the earnings release, the earnings guidance remains unchanged:

"Our fiscal second-quarter EPS came in stronger than anticipated. Some EPS strength in the second quarter reflected some volume that we were expecting early in the fiscal third quarter, and we still expect good comparable EPS growth in the second half of fiscal 2014. Challenging industry conditions make us cautious about the near term, and our 2014 EPS guidance reflects this. Taking our strong second-quarter EPS performance and the industry environment into consideration, we are reaffirming our EPS goal in the range of $2.34-$2.38, adjusted for items impacting comparability."

Upside Potential, Time Horizon, Downside Risk

I usually calculate upside potential and downside risk from the midpoint of my recommended buy range, but in this case, I use the top of the range. I've done that because the bottom of the range is further below current price than usual and I think it is unlikely to be reached, but it is worth noting since it may be more appropriate for some investors, depending whether they are initiating new positions or adding to existing holdings.

The table below includes the current-year EPS estimate of $2.34 and the 8.7% next-five year EPS growth rate used in my valuation calculations. Both figures are the mean of 15 estimates, and it's also worth noting that the projected EPS growth rate for next year is 10.70%. In order to value the stock conservatively, I used a 12% discount rate and a 4% terminal growth rate. The calculations return a fair value of $36.90, which is one basis of my twelve-month $36 price target (12.5% above $32).

(click to enlarge)

Another reason for my $36 price target is because CAG is currently at a significant discount to most of its peers on a relative valuation basis. Even after the post-earnings rally, CAG is still at a forward P/E of only ~12.9x, while General Mills (GIS) trades at a ~15.7x forward P/E, Kraft (KRFT) ~16.9x, Mondelez (MDLZ) ~20.2x and Unilever (UL) ~17.5x. Granted, that isn't an apples-to-apples comparison since each company has unique positives and negatives. However, if CAG just regains a 14x forward P/E (its pre-acquisition 10-year median), the share price would be $36.12.

I consider annualized return above 10% (excluding dividends) worthwhile for conservative income investors seeking relatively low-risk stocks. With those qualifying conditions, and a ~2.98% dividend yield, I believe CAG is a good buy for long-term investors. Even though the stock doesn't appear to be extremely undervalued for the near term, I believe that it is from a longer-term perspective. In fact, I expect an earnings improvement trend to be established and may raise my $36 price target within its 12-month time frame. I don't have a staff to assist with researching and reworking my analyses, so I usually only raise targets if the increase is at least 10% annualized. For example, at the midpoint of the 12-month time frame, raising my CAG target 5% over my current $36 target would make it $38.

I don't see much downside risk with CAG since the stock already took quite a beating since the company lowered current fiscal year guidance from $2.40 to a $2.34-$2.38 range, which it reaffirmed last week. Absent a more extreme event, whether company specific or general, we have already seen that CAG is unlikely to go much below $30 (6% below $32).

My specific plan and recommendation is to buy half of the amount I want to add to my position on the next dip to my buy range, then stand ready to buy the other half upon the next indicator that a trend of improvement is developing. A few potential indicators are covered in the next section.

Opportunity Realization Drivers

With $18 billion in annual sales, the combination of ConAgra and Ralcorp (RAH) created the second largest packaged-food company in the U.S. by sales, trailing only Kraft with $19 billion. With RAH bringing an additional 10,000 employees into the CAG fold, which now totals over 36,000, few would argue that this is not a very large and complex acquisition.

I've worked at a large company that made a major acquisition and, since I had worked at the company many years prior and had an interest both as an employee and a shareholder, I observed and studied the situation closely via a unique inside view. In fact, I have had unofficial discussions about the subject directly with directors including a CEO and a Chairman. One of the many things I witnessed and learned is that integrating a large acquisition consumes all of an entire management team's time for 2-3 full years. Integrating two large corporations is a huge undertaking, but like most things, the reward tends to be commensurate with effort. Perhaps the only problem is that we live in an instant-gratification culture that defines any less than immediate success as failure, not progress. My point is that nine months (the time from the closing to the Q1 earnings report) is hardly a reasonable time frame to judge the success of the RAH deal.

This excerpt is from the original announcement: "ConAgra intends to use its strong infrastructure and productivity capabilities to drive significant cost synergies from this transaction, primarily in the areas of supply chain and procurement efficiencies. It expects to achieve approximately $225 million of cost synergies on an annual basis by the fourth full fiscal year after closing." (Note: the $225 million has been revised to $300 million.)

Considering the "by the fourth full fiscal year after closing" phrase in that statement and the fact that less than one fiscal year has passed since the January 2013 closing, perhaps CAG hasn't actually performed as poorly as some perceive. Perhaps that is even more evident if we consider that CAG closed the RAH acquisition two full years after pursuing the need to make such an acquisition. It seems CAG knew years ago that it needed to make strategic moves to secure its competitive position and continue growing, but ended up years behind its accurate foresight by no fault of its own.

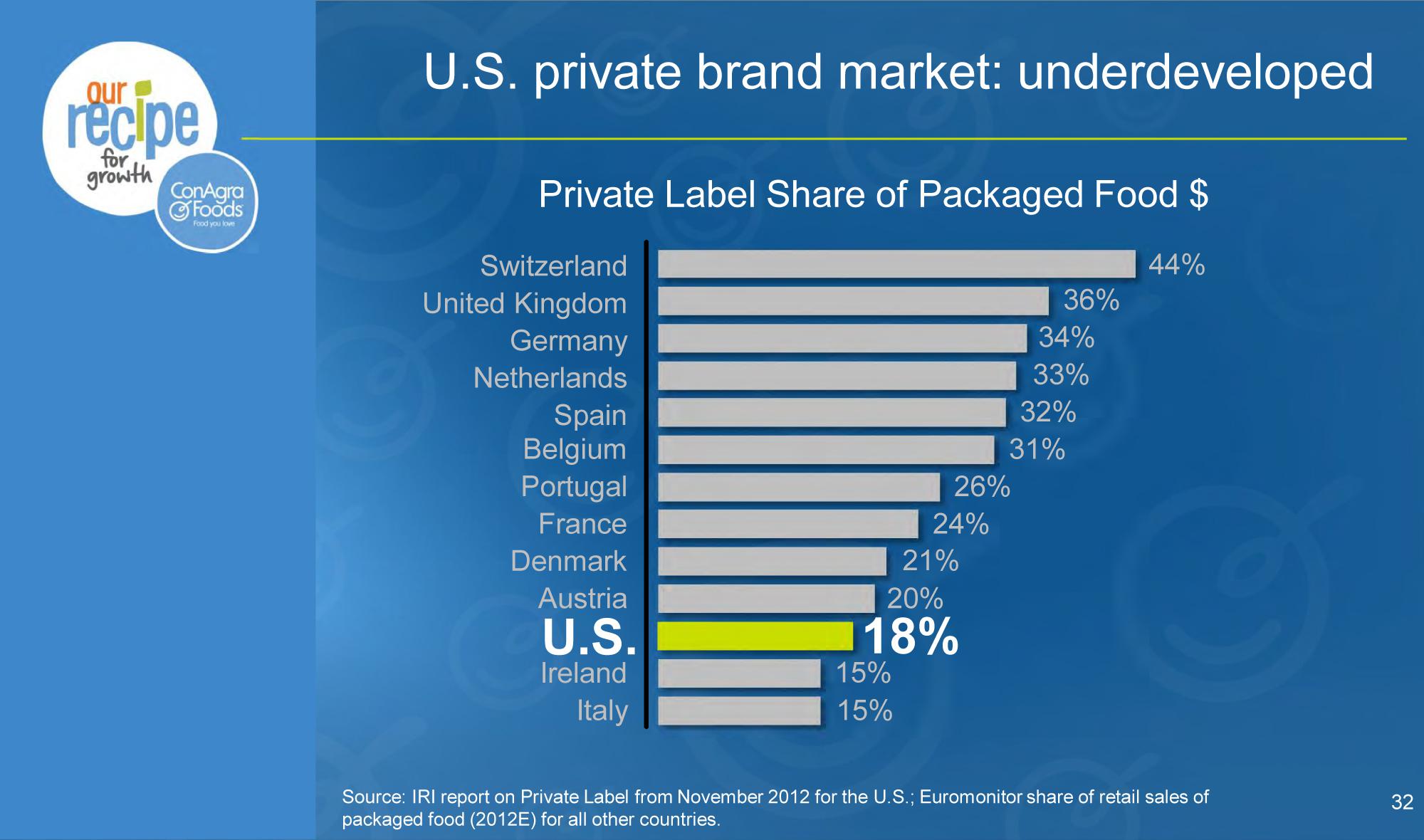

As the slide below shows, the U.S. private-label market is actually very underdeveloped, leaving lots of room for the new CAG to grow. In fact, perhaps that is at least partially because the market was underserved by a company that clearly did not have the infrastructure, leadership or other resources to handle it. Lest we forget why companies get acquired in the first place -- they have assets worth significantly more than the value they have been able to extract. In other words, companies are not necessarily at their best when they are acquired and very typically take time to lift to the efficiency level of a truly competitive company.

(click to enlarge)

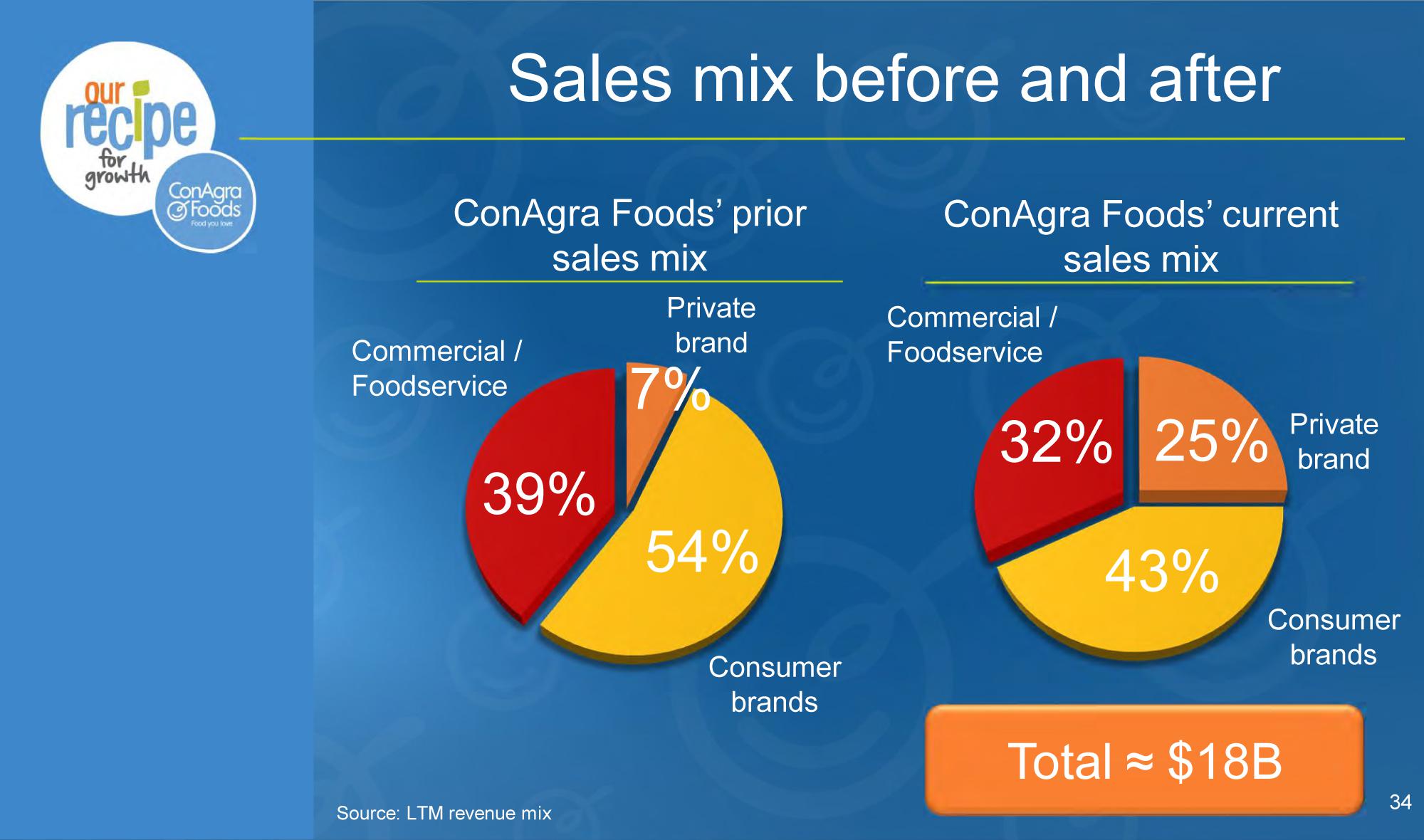

As the slide below shows, the RAH acquisition is helping CAG reposition to take full advantage of the underserved private-label market. For example, as CEO Gary Rodkin pointed out early in the process of acquiring RAH:

"While private-label foods may have slowed as a whole, growth is occurring in certain categories, like snacks, and at retailers like Whole Foods Market (WFM ), Costco (COST ) and privately-held Trader Joe's, which devote extra attention to their store brands. Two of Ralcorp's key customers are Costco and Trader Joe's."

(click to enlarge)

In retrospect, the CAG selloff that hit a trough on October 8 was a great opportunity to open a new position or add to an existing position. But, like many investors, I first wanted to see hard evidence of a course correction.

It appears that is exactly what we got last week. I think CAG shares will gradually resume momentum over the coming 6-9 months as it becomes more clear that projected revenue and earnings, as well as cost synergies, from the January 2013 Ralcorp acquisition are indeed coming to fruition.

Before the next earnings report in late March, the first predictable catalyst for CAG will be the company's presentation at the February conference for the CAGNY (Consumer Analyst Group of New York). It's certainly possible, if not likely, that there will be analyst upgrades prior to that presentation, but the CAGNY conference is a more predictable event to watch for.

Catalysts to look for include changes to any of the main points ConAgra CEO Gary Rodkin made during last week's conference call such as:

"We continue to be committed to delivering $0.25 of accretion in EPS this fiscal year from the Ralcorp deal. And we also remain committed to our short-term and longer-term synergy estimates, which are on track to deliver. Just as a reminder, the accretion and synergy benefits will show up across all of our business segments."

"We're on track for our fiscal 2014 EPS commitments, meaning a year of 8% to 10% growth, despite a continued challenging environment that has been a bit difficult to forecast. While some drivers and timing of our performance are a bit different now than our earlier plans, we're confident in the earnings outlook. We understand the levers we have to pull to deliver, given our focus on cost savings, synergies, strong customer partnerships and overall execution. I firmly believe we're setting up ConAgra Foods for long-term success, despite some bumps in the road, and that we're in a great position to deliver our fiscal 2015 to 2017 EPS and synergy targets."

Risk Factors

1. Debt Financing

As discussed in my recent article about technology company Perficient (PRFT), acquisitions involve risks in two ways: business integration risk and financing risk. Business integration issues were discussed above so I'll now focus on financing risk or, more specifically in the case of CAG, debt.

As of the reported quarter, CAG total net debt was ~$9.4 billion, the vast majority of which is new debt from the $6.8 billion RAH acquisition. While that is clearly a substantial amount of debt and worthy of keeping an eye on, I do not find it overly concerning for a number of reasons including:

- necessary and worthwhile use of debt

- relatively long-dated debt maturities

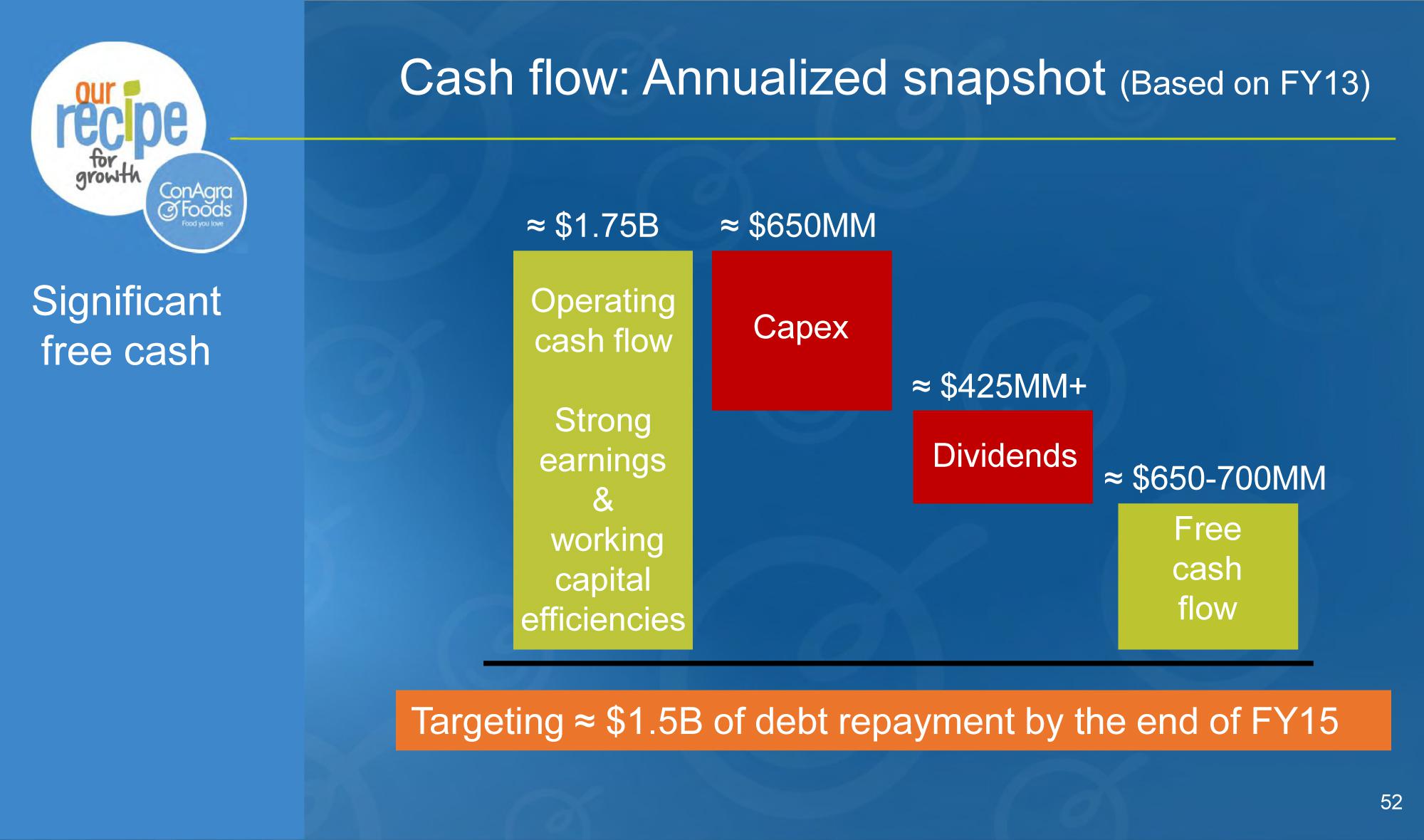

- particularly strong free cash flow [FCF] generation

- aggressive cost management initiatives

- plan to manage debt and focus on that plan

CAG has repeatedly stated its capital allocation priorities as follows:

- near term -- debt repayment & maintain strong dividend

- long term -- dividends, M&A, share repurchase & debt repayment

As Chief Financial Officer John Gehring reaffirmed during the recent conference call:

"On capital allocation, our priority over the next couple of years continues to be the repayment of debt, as well as strengthening our credit metrics. Consistent with that priority, we currently expect to repay approximately $600 million of debt in fiscal 2014 and a total of $1.5 billion by the end of fiscal 2015. These amounts exclude any additional repayment that we expect to fund from the cash proceeds related to the Ardent Mills transaction."

Fitch Ratings seems to agree that CAG has the wherewithal and a good strategy to service its debt:

"The company's commitment to deleverage, free cash flow generation, ample liquidity, and the strength of this strategic combination support the ratings. Debt Reduction, Synergies Achievable: ConAgra plans to prioritize its FCF to repay a total of $1.5 billion of debt through fiscal 2015. Fitch conservatively estimates ConAgra's FCF at approximately $500 million this fiscal year. Thus, the company may need to utilize a portion of its cash to achieve its targeted debt reduction of at least $600 million this year. The company also plans to maintain its current dividend and keep share repurchases modest so the focus remains on debt reduction."

"Fitch estimates that ConAgra's leverage (total debt to EBITDA) should decline to the low 3x level or below by the end of fiscal 2015. Adequate Liquidity, Manageable Maturities: ConAgra maintains an undrawn $1.5 billion revolving credit facility that provides backup to its commercial paper [CP] program. ConAgra had $280 million CP outstanding and $194 million cash at August 25, 2013. Subsequent to the end of the quarter, ConAgra extended its revolving credit facility by two years to September 14, 2018. At August 25 2013, ConAgra had $900 million outstanding on its term loan which matures January 29, 2018. The company intends to pay off the balance by the end of fiscal 2015. ConAgra plans to refinance its $500 million 5.875% notes due April 2014. Additional maturities include $250 million 1.35% notes due September 2015."

I think one of the biggest mistakes many retail investors make is defining corporate debt the same way they look at their personal debt -- through the lens of otherwise admirable "live within your means" principles. The main flaw in that theory is that, with the possible exception of education loans, personal debt does not invest in assets that generate income ... at all, let alone income that is many times the debt cost. So, corporate debt is not inherently bad. Considering the various factors listed, CAG appears well-equipped to manage its debt and appropriately focused on doing so.

As a final note on this subject, the CAG enterprise multiple (EV/EBITDA) of 9.4 is not only significantly lower than the peer group average of 11.4, but also significantly lower than any of the individual peers in the group.

(click to enlarge)

2. Potential Litigation Liability

W.P. Fuller & Company, a defunct paint company that dated back to the 1850s (no, that's not a typo), apparently sold paint made with lead at some point after lead was deemed unsafe (1978). Although it's actually easier to find associations between the long-gone W.P. Fuller and today's Valspar (VAL), CAG indirectly acquired some W.P. Fuller assets through a series of acquisitions that took place decades ago. Last week, a California judge proposed a decision that concludes CAG assumed all legal liabilities of W.P. Fuller and is, thus, liable for a portion of the proposed $1.1 billion ruling against three companies. CAG is appealing the proposed ruling.

While I'm not an attorney, this appears to be a cash-strapped state trying to fix its many problems by overreaching into the pockets of corporations. If the proposed ruling does stand, which there are reasons to doubt, I still would not consider it a significant risk to CAG for several reasons. First, at risk of sounding crass, an approximate one-third portion of $1.1 billion is a drop in a bucket for a $14 billion company with annual free cash flow of ~$0.5 billion. Perhaps more importantly, corporations carry insurance for legal liabilities. Another reason this doesn't affect my opinion of CAG is because I'm an investor, so relatively minor one-time events don't affect the time periods that interest me. This doesn't even affect my short-term price target for CAG since one reason I use conservative valuations is to leave room for unforeseeable events that can come up with any company. I think the only real risk related to this is the potential to set precedent.

3. Potential Consumer Weakness

As discussed in my article about Kroger (KR), reductions in SNAP benefits (the Supplemental Nutrition Assistance Program known as food stamps) could impact the entire retail industry since food purchases take priority over other retail items such as clothing. However, some families that are already struggling may not be able to divert money from other needs to buy food, so the cut in SNAP benefits could still affect the food industry. The reduction in SNAP benefits took effect very recently so the potential impact on the food industry is unknown. With that said, it seems that the most likely outcome will be some consumers who rely on SNAP benefits may trade down from some branded products to store-brand products. I don't believe this issue will significantly affect CAG performance since the company is now a leader in both categories due to the Ralcorp acquisition. So, I think the SNAP benefits reductions will be a wash for CAG.

As with all investments, there are indeed risks, but I consider CAG a very good long-term holding and plan to continue adding to my position.

I'd love to hear from other CAG shareholders in the comments section.

I researched and wrote this article 12/19-12/22. Thank you for reading.

Disclosure: I am long CAG, KR. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

Additional disclosure: I am long CAG and KR, and may buy additional shares at any time.

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire