Alliance Fiber Optic Products Inc. (AFOP) appears at first glance to be not relatively but absolutely attractive to certain equity-market participants who focus on growth and value, given that 2013 Nobel Prize-winning economist Robert J. Shiller's cyclically adjusted price-earnings ratio is currently at the lofty level of 25.08. As Aesop fabulously observed in "The Wolf in Sheep's Clothing," however, appearances often are deceiving.

AFOP has had a great year. During the first three quarters, the company's revenue rose to about $54.27 million from about $34.45 million year on year and its earnings per share rose to 65 cents from 22 cents on the same basis. Adjusted for the firm's two-for-one stock split in September, its closing share price has ranged between a 52-week low of $5.32 on Jan. 30 and a 52-week high of $22.99 on Sept. 19. And, at the close of the trading session Thursday, its P-E ratio was a seemingly reasonable 15.51.

Nonetheless, both growth-and-value factors may have certain investors hunkered down in the bunkers during the battle between the bulls and the bears over this name. According to Nasdaq.com, insiders own about 34.1 percent of AFOP and institutions own about 28.8 percent of the company. Meanwhile, the same source reported the short interest on Nov. 15 was 2,619,509 shares, the highest of the year.

(click to enlarge)

Source: Alliance Fiber Optic Products Inc.

The Business Of Alliance Fiber Optic Products

Based in Sunnyvale, Calif., AFOP designs, manufactures and markets fiber-optic components for communication-equipment manufacturers and communication-service providers. The company generally categorizes its offerings in one of two segments, either connectivity products or optical passive products. The firm makes most of its connectivity products at its facility in Tu-Cheng City, Taiwan, and all of its advanced and filter-based products at its facility outside Shenzhen, China, according to the U.S. Securities and Exchange Commission Form 10-K it filed March 20.

In the same document, AFOP reported: "Recent orders for our products have been utilized both for upgrades of existing networks and new network builds. In addition, certain large telecommunications service providers have recently begun to deploy new broadband access networks based on fiber optic technologies for residential users. These fiber-to-the-home networks, or FTTH, are expected to significantly increase the capacity and expand the types of services that can be utilized by residential users."

However, AFOP added at that time, "It remains difficult … to predict the timing or extent of a full industry recovery and the potential impact to our business from this or any other deployment initiatives."

This difficulty in forecasting notwithstanding, AFOP has indicated the strong demand for its offerings has continued into the fourth quarter, with CEO and President Peter C. Chang anticipating on Oct. 24 the company may book between $21.50 million and $23.40 million in revenue during the current period, according to the firm's Q3 earnings-call transcript at Seeking Alpha. By way of comparison, it recorded revenue of about $12.16 million in Q4 last year and about $23.07 million in Q3 this year.

OK, AFOP's recent revenue figures are impressive. But they come in a context described well in the company's SEC Form 10-Q on Nov. 13.

During Q3, AFOP's 10 biggest customers accounted for 79.1 percent of revenue this year and 66.3 percent of it last year. Over the same period, the company's largest customer accounted for 40.1 percent of revenue in 2013 and 14.1 percent of it in 2012. A concentration of risk of this kind makes a certain sort of investor as jumpy as the proverbial cat in the proverbial room full of those proverbial rocking chairs.

(FYI: Bruce Pile, another contributor to Seeking Alpha, covered details of AFOP's line of business in his "Alliance Fiber Optic And The New Networking" last week.)

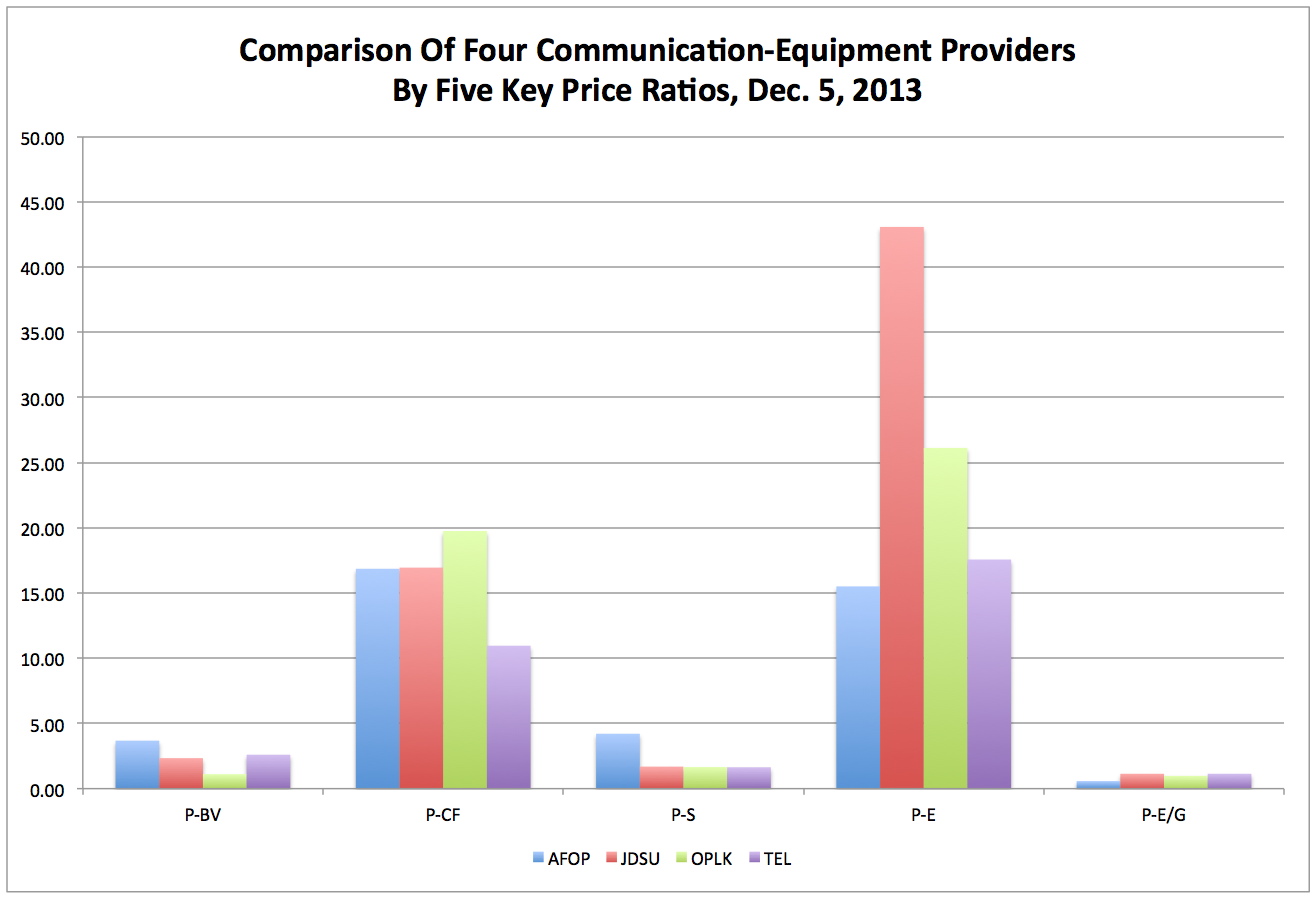

(click to enlarge)

Sources: Prepared after the market close Thursday, this chart incorporates price-to-cash flow (P-CF) data from MSN Money and price-to-book value (P-BV), price-to-sales (P-S), price-to-earnings (P-E), and price-earnings-to-growth (P-E/G) data from Yahoo Finance.

The Valuation Of Alliance Fiber Optic Products

Bearing in mind AFOP's share price closed at $15.09 Thursday, proprietary fundamental analysis suggested the stock was worth $12.47 a stub the same day. Of course, proprietary fundamental analysis can be in error for all kinds of reasons, including one as simple as a bad cell in a spreadsheet (especially the dreaded A1). Therefore, it was accompanied by a comparison of five key price ratios relevant to the company and three of its competitors in the communication equipment industry.

AFOP mentioned in its SEC Form 10-K it had more than 20 competitors and named five of them: JDS Uniphase Corp. (JDSU), Oclaro Inc. (OCLR), Oplink Communications Inc. (OPLK), the privately held Senko Advanced Components Inc., and TE Connectivity Ltd. (TEL). Because Senko Advanced Components is privately held and Oclaro is unprofitable, they were excluded from the comparison of price-to-book value (P-BV), price-to-cash flow (P-CF), price-to-sales (P-S), price-to-earnings (P-E), and price-earnings-to-growth (P-E/G) metrics.

As the above chart shows, AFOP appears cheap by two of these ratios, dear by two of them, and somewhere in the middle of the pack by the fifth. The stock seems inexpensive with P-E and P-E/G ratios of 15.51 and 0.58, in that order, and it seems expensive with P-BV and P-S ratios of 3.68 and 4.21, respectively. Meanwhile, it seems neither/nor with a P-CF ratio of 16.86.

Because of the concentration of risk to growth represented by AFOP's biggest customer accounting for 40.1 percent of revenue in Q3 and because of the hues of the valuation picture painted here, the company's equity is not absolutely but relatively attractive to certain stock-market participants who focus on growth and value.

If AFOP Continues To Grow, Then It Could Merit Its Valuation

AFOP's strong balance sheet on Sept. 30 showed about $45.67 million in cash, cash equivalents and short-term investments versus about $18.88 million in total liabilities, which may allow the company to announce a new share-buyback program to either complement or replace the $6.00 million share-repurchase program it launched a couple of years ago. About $0.02 million was remaining under this repurchase program on Sept. 30.

More immediately, the balance sheet is allowing AFOP, with a market capitalization of about $276.68 million, to deliver this month an annual dividend of 15 cents per share to stockholders of record on Friday, as the firm reported in a SEC Form 8-K on Nov. 7. The company has about 18.34 million shares outstanding, so the cost of its dividend should be about $2.75 million.

Buybacks may be nice, and dividends may be nice, but certain growth-and-value investors may await more clarity about AFOP's anticipated revenue during 2014 before paying its current share price. Such clarity might come when the company reports its Q4 financial results, presumably late next month. Meanwhile, the growth-and-value types likely will be engaging in a bit of watchful waiting, on the lookout for share-price weakness that would allow them to possibly acquire the stock with a bigger margin of safety, probably by selling a put or puts.

Many risks associated with AFOP as an investment vehicle are well described on pages 8-16 of the company's SEC Form 10-K, and a few risks associated with anything as an investment vehicle include changes in the easy-money policies of the U.S. Federal Reserve and other central banks around the world. Along this line, it is important to note the Federal Open Market Committee will conduct its next meeting on Jan. 28-29, which is around the time AFOP is expected to report its Q4 financial results.

Disclaimer: The opinions expressed herein by the author do not constitute an investment recommendation, and they are unsuitable for employment in the making of investment decisions. The opinions expressed herein address only certain aspects of potential investment in the securities of any companies mentioned and cannot substitute for comprehensive investment analysis. The opinions expressed herein are based on an incomplete set of information, illustrative in nature, and limited in scope, and there are limitations to their accuracy. The author recommends all investors conduct detailed investment research of their own, including review of relevant SEC filings and consultation with a qualified investment adviser. The information upon which this article is based was obtained from sources believed to be reliable, but it has not been independently verified, which means the author cannot guarantee the accuracy of this information. In addition, the opinions expressed herein reflect the author's best judgment as of the date of publication, and they are subject to change without notice.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

from SeekingAlpha.com: Home Page http://seekingalpha.com/article/1882701-alliance-fiber-optic-products-whats-it-worth?source=feed

Aucun commentaire:

Enregistrer un commentaire