Attempting to catch a falling knife is a fool's errand, but picking one up off the ground is a different story. Imris Inc.(IMRS) is a Canadian medical device company that specializes in developing, manufacturing, and marketing surgical theatres for hospitals. The company's stock has been on a rollercoaster since its IPO on the NASDAQ in 2010, falling from a high of $8.78 to today's share price of $1.33.

(click to enlarge)

With a new CEO in place, recently launched business initiatives, and an all-time low stock price, Imris is in turnaround mode and seems to be developing a bottom. Improving fundamentals and continued revenue growth signal that this knife is ready to be picked up off the ground.

The intimidating challenge of selling capital-intensive surgical platforms to cash strapped hospitals is now less daunting with management's recently launched multi-source sales program, which should help speed up the decision process and lessen the cost for Imris's potential customers. With a focus on intra-operative MRI's and other visualization techniques, Imris is carving itself out as a niche player in the surgical market and should begin to see increased traction as the company introduces new products and reduces costs for their customers through its new sales initiative.

The Product

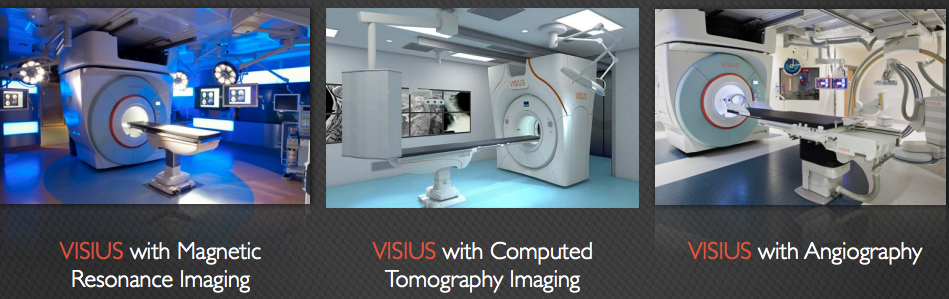

Imris focuses on providing state of the art image guided therapy systems to hospitals. Their main product is the Visius Surgical Theatre, a 2-3 room operating theatre that houses various equipment which comes in different formats and configurations. The main advantage of the Visius Surgical Theatre is the ability to conduct real time visualizations such as an MRI in the middle of a surgical procedure without moving the patient. Below is a picture of a typical operation room utilizing the Visius Theatre, and here is a video that walks you through the room.

(click to enlarge)

Depending on the surgical theatre, an MRI, Angiography, or Computed Tomography can be conducted in the middle of an operation. The recently launched iCT is the first ceiling mounted CT scanner in the world that decreases radiation exposure when compared to current CT imaging systems. Currently, Imris is developing two therapy platforms, a surgical robot named the Symbis Surgical System, and a system that allows for MR guided radiation therapy thanks to a partnership with Varian Medical (VAR). The company's belief is that improved patient outcomes and reduced costs of care can be achieved through the combination of enhanced visualization and therapy deliveries, and there is data to back this up. 86% of surgical tumor procedures utilizing intra-operative Magnetic Resonance Imaging (iMRI) removed the entire tumor , compared to just 53% for operations not using iMRI.

Any traditional surgery to treat a number of complications and conditions can be conducted in a Visius Surgical Theatre. The company is specifically targeting brain, pituitary, and spine procedures, which total more than 3.5 million procedures worldwide. The Symbis Surgical System will be specifically targeting neurosurgical and spinal operations, which amounts to more than 2 million procedures worldwide. Clearly, the market potential for Imris is massive, but with only 60 Visius Surgical Systems installed to date Imris has a long way to go before obtaining just a sliver of the pie.

New Sales Initiative Will Spur Growth

The biggest challenge for Imris has been closing deals. The company's sales have been stagnant for a while, due to long, drawn out decision delays. In the past year Imris has sold a total of five Visius Theatres, and usually completes one sale per quarter. The sales cycle is lengthy, and because of the systems high price tag and large footprint, many different groups are involved in the decision making process at hospitals. The company sold one Visus Surgical System during Q3 2013.

To address this issue, recently hired CEO Jay Miller implemented a multisource sales initiative that allows customers to obtain specific components of the Visius Surgical Theatre directly from qualified OEM partners at a lower cost. The program commenced last quarter for customers who had delayed their purchasing process. While this may sound foolish to the common businessman, it's not. Hospitals are still required to commit to a long term service contract with Imris, Imris still completes the installation of the system, and instruments and accessories are still purchased from Imris. This has moved the sales process forward for a number of potential customers, who are now in the late stages of the decision process. The cost savings under this new approach make purchasing a system more flexible and realistic for a hospital and its budget. Partially removing the middleman (Imris) will pave the way for increased sales and should result in higher revenues for the company as more and more service contracts are signed.

The Business Model

Imris's business model is identical to that of other surgical platform companies with similar products, such as Intuitive Surgical's (ISRG) Da Vinci system and TransEnterix's (OTCQB:TRXC) Surgibot. The Visius System has an initial price tag of $3 to $7 million for the iMRI model, and $1.5 to $3.5 million for the recently launched iCT model. The company expects to generate revenue from the iCT by the end of 2013. Customers must sign a service contract, which has an average cost of $300,000 per year, and usually entails a minimum commitment of 4-5 years. The company also collects revenue from instruments and accessories that are utilized during operations; these cost approximately $1,000 per procedure. As the company begins to commercialize more surgical products and sell more systems, the recurring revenue stream will become more predictable, robust, and will significantly contribute to the company's financial position.

The Symbis Surgical System will cost roughly $2 million, have an annual service contract of approximately $200,000 per year, and cost roughly $1,200 in instruments and accessories per procedure. The company expects the Symbis System to receive FDA clearance and be ready for commercialization around 2016. This is still an early stage product, but the Symbis Surgical System will be an ideal fit for the already installed Visius Theatre base because it will be the first surgical robot in the world that is compatible with MR and CT imaging systems. This should offer many unique advantages to both the surgeon and patient.

Why Imris Can Propel Higher

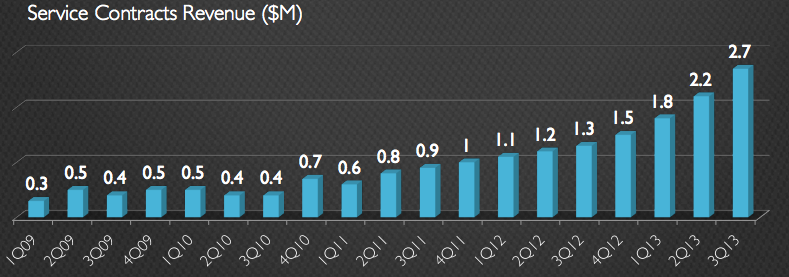

Imris has a sales funnel of more than $500 million, which makes booking orders a primary goal for the company. As more orders are booked, revenues will jump and service revenues will continue to grow at an increasing rate.

(click to enlarge)

In Q3 of 2013, Imris increased revenues by 54%, and service revenues by 108%, compared to the year prior. The company's Q3 EPS stood at -$0.07, a 63% improvement over the year prior. The company's backlog continues to stand above $100 million, gross margins are increasing, and the company's financial health has been improving quarter after quarter.

Because of the high selling points of Imris's products, one sale can increase revenues by up to $12 million. Therefore, if the company manages to book more than one order in a quarter, a surge in revenues and surprise to Wall Street could occur. This is highly likely now that Imris has rolled out a new sales approach and has introduced its new iCT system. With several hospitals now in the late stages of the decision making process, a blowout quarter may be right around the corner for Imris.

The sale of one Visius System represents an average of $6 million in revenue, followed by an average of $300,000 paid annually for a minimum of 4-5 years, and an average of $130,000 worth in accessories per year at today's current operation rate. Therefore, the sale of one Visius Sugical Theatre represents an average revenue of $8 million over the 5-year contract, and higher end systems can reach more than $15 million in revenue over a 5-year contract. These types of numbers are massive for just one order, and should significantly boost annual revenues past the current level of $50 million as more orders are booked.

Imris is gearing up for strong growth, after recently relocating its business from Canada to Minnesota. The reasons behind this move were highlighted in the last conference call, and point to further expansion in the future. CEO Jay Miller stated:

Not only will we be manufacturing and shipping iMRI systems, but we expect that over time we'll be shipping and manufacturing significant volume of iCTs. On top of that over time, we expect we will be shipping robotic systems as well and on top of disposables. So we will have more things where we will need more space, which is exactly why we took on the space in operations that we did.

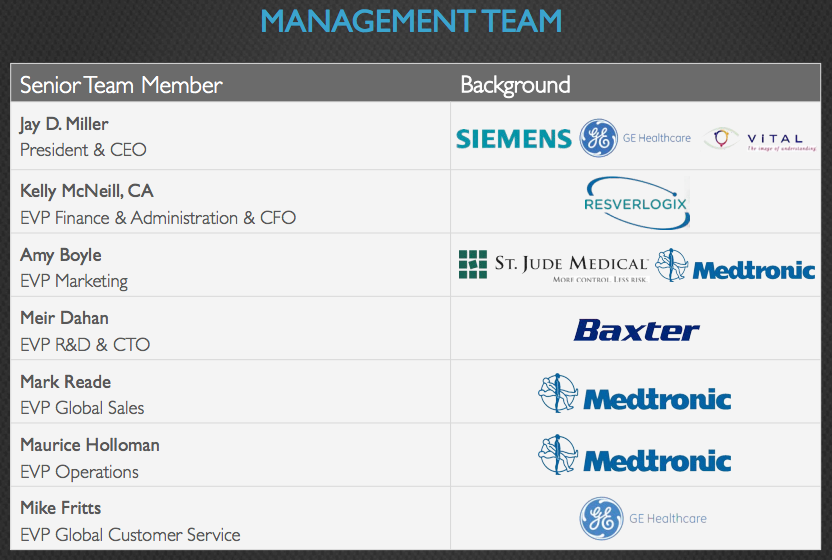

The company has experienced management in place who are capable of executing Imris's business plan. Jay Miller was the former COO and President of Imris and took over as CEO this past summer, replacing founder David Graves.

(click to enlarge)

Patent Portfolio

Imris owns 100% of its intellectual property, which includes more than 50 patents either already issued or pending in the U.S. and Canada. These patents don't expire until 2030, and cover integral parts of the Visius Surgical Theatre. Some of the granted patents cover image-guided intervention, the use for automated medical robotics, MR-guided radiation therapy, and the ability to image when MR is positioned. These are high valued patents that protect advanced technology and act as barriers of entry to competing companies.

Valuation

Currently, Imris has a market cap of $67 million, generates annual revenue of more than $50 million, and has ~52 million shares outstanding. If Imris begins to execute its business plan and increase sales through their new sales initiative, then shares should experience a sharp reversal. If Imris manages to sell one and a half Visius System per quarter, and one ceiling mounted CT scanner every quarter, with service revenues and revenues generated from instruments and accessories remaining flat, then yearly revenues for Imris could reach approximately $100 million. At 1x sales, this would move IMRS' share price to roughly $1.92, representing 45% upside when compared to today's level. Utilizing Imris's current price/sales multiple of 1.22X revenues would equate to $2.34 per share, and a 2X multiple would equal $3.84 per share.

Risks to Consider and Potential Downside

Imris Inc. is a small cap company that is highly volatile and subject to all risks related to said companies. The company has an accumulated deficit of more than $100 million and has yet to turn a profit. Competition is also intense as hospitals opt for cheaper visualization devices that are less capital intensive than Imris's products.

The practice of selling expensive platforms to cash strapped hospitals will continue to be an obstacle for the company, and Imris's high priced products are a double edged sword. If the company manages to book more than one order per quarter revenues would soar, but any delay or the cancellation of just order would lead to a significant drop in revenues and share price. Shares of Imris are down 65% YTD, and hit an all time low of $1.16 after disappointing earnings were released in early November.

The initial revenues generated from the sale of one Visius Surgical System represent ~$0.12 per share. Based on a 2X multiple, the failure to sell a Visius System would result in a drop of $0.24 per share. At today's current prices, shares would drop to $1.09 if Imris disappointed investors and failed to sell any systems in a quarter. Therefore, if Imris fails to sell any systems during Q4 2013, the potential downside is approximately 18%.

The recently launched iCT system represents approximately $0.06 per share for every unit sold. Imris would have to sell two iCT systems to make up for the lost revenue of one Visius Theatre. Since Imris expects to book sales of their iCT system by the end of 2013, any potential drop in Visius revenues should be offset by revenues generated from the iCT. If Imris only manages to sell one iCT system and zero Visius system's from Q4 2013, then shares could see a potential downside of 9%. The sale of two Visius Systems and two iCT systems for Q4 2013 would represent potential upside of 55%. With a book value of $1.07 per share, Imris has more upside than downside potential.

Conclusion

Imris has come a long way since it re-branded its Visius Surgical Theatre in 2011. At the end of Q3 2013, Imris had sufficient funds to continue operations for more than a year without the need for raising additional capital. Imris should begin to see an increase in business as their recently established partnerships with medical companies Varian Medical and Siemens Healthcare (SI) lead to new distribution channels and increased sales. The company's new sales initiative and recently launched CT scanner should lead to immediate revenue growth that will continue to improve the company's financials, offer predictability of revenues with an increase in recurring service contracts, and lead to eventual profitability. At current prices of $1.33, Imris' risk/reward profile makes a compelling investment for speculators who believe the company and its new CEO will be able to turn around the company and begin to increase bookings.

All information was sourced from the company's investor presentations, conference calls, and SEC filings found here.

Disclosure: I have no positions in any stocks mentioned, but may initiate a long position in IMRS over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire