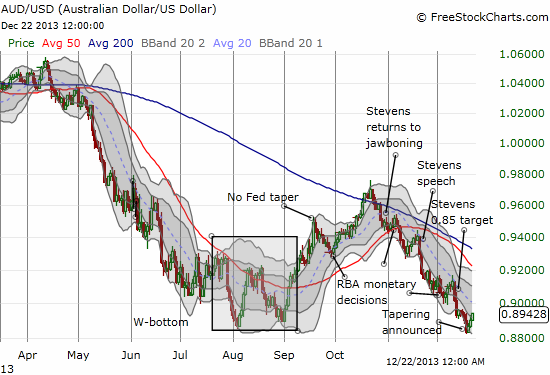

The Australian dollar (FXA) has finally retested the "W-bottom" from August of this year. So far the test seems successful as the Australian dollar has sharply bounced off the lows over the past three days.

(click to enlarge)

Stevens helps to drive the Australian dollar downward

Source: FreeStockCharts.com

One of the more notable features of AUD/USD is how well it has responded to the jawboning of Governor Glenn Stevens. His active verbal intervention into the currency reached a climax when on December 12th he fixated the market's attention on a downside target of 0.85 for the Australian dollar versus the U.S. dollar:

To the extent that we get some more easing in financial conditions, at this point it's probably more preferable for that to be via a lower currency at the margin than lower interest rates…I thought US85¢ would be closer to the mark than US 95¢, but really, I don't think we can be that precise.

With a housing market that is heating up again, it makes a lot of sense that Stevens would prefer a lower currency to more rate cuts. More rate cuts would likely drive more speculative loan activity in real estate. A lower currency might slow down speculation to any extent that it is driven by foreign capital.

The Australian dollar immediately took a dive on Stevens' target, but it took a few days for the market to respond to the implication that rates are not likely going to get cut at the February RBA meeting. On December 12th, the RBA Rate Indicator suggested 23% odds of a rate cut. It did not start falling until December 16th. The odds now sit at a more reasonable 12%.

(click to enlarge)

Expectations for a rate cut take a tumble

Source: RBA Rate Tracker

{kind=link}

Interestingly, the accelerating weakness in the Australian dollar did not help the Australian stock market this time around like it seemed to do earlier in the year. The ASX200 slid sharply from November to mid-December. The recent rebound has occurred as the Australian dollar seems to have hit some kind of bottom.

(click to enlarge)

The Australian stock market seems to have finally ended a 6-week skid

Source: ASX

The bounce in the Australian dollar and the Australian stock market also happens to coincide with the announcement from the Federal Reserve that it will finally begin to taper its bond purchases. Governor Stevens and the RBA have repeatedly indicated that they are looking forward to a normalization of U.S. monetary policy under the assumption that it would help to lower the value of the Australian dollar as it becomes less attractive in relative terms. So why the bounce now that the Fed has seemingly delivered? Probably a sudden reversal in interest rates. The tapering announced by the Fed is more like a "sampling" sugar-coated with the promise of easy money for a long as the eyes can see:

The Committee now anticipates, based on its assessment of these factors, that it likely will be appropriate to maintain the current target range for the federal funds rate well past the time that the unemployment rate declines below 6-1/2 percent, especially if projected inflation continues to run below the Committee's 2 percent longer-run goal.

Indeed, the yield on the 10-year U.S. Treasury bond (TLT) ended the week at its lowest point for December. Hat tip to Ilya Spivak who posted the following chart on StockTwits demonstrating the tight correlation between (inverted) U.S. bond yields and the Australian dollar. (Usually the spread between bond yields in the two countries provides a more accurate indicator, but here, the U.S. bond yield is sufficient).

In 2013, the Australian dollar's fate has been closely tied to that of the U.S. 10-year Treasury bond yield.

It seems that if Stevens really wants to drive the Australian dollar closer to his 0.85 target, he WILL need to further lower rates. If the Australian dollar remains so closely bound to the 10-year bond yield, even creative jawboning may not be enough.

Early this year I was still in the habit of correlating the Australian dollar to the S&P 500 (SPY) and using the Australian dollar as an early indicator of direction for the index. That correlation completely broke down once the Reserve Bank of Australia (RBA) cut rates on May 7th from 3.0% to 2.75%. The Australian dollar declined rapidly for the next three months, only stopping after, ironically enough, the RBA cut rates one more time without strongly hinting it might do so again. While the S&P 500 made a complete roundtrip from a rally in May to a sell-off in June, by the time the Australian dollar bottomed, the index was about 7% higher from the time of the RBA's May rate cut.

So, for now at least, it seems clear that the proper correlation is between the Australian dollar and U.S. bond yields and NOT the U.S. stock market. This relationship should be a key metric to watch for 2014.

I conclude with an updated chart showing how the S&P 500 has trended higher all year almost oblivious to the churning and gyrations of a number of possible correlates:

(click to enlarge)

The S&P 500 has risen far above the fray this year

Source: FreeStockCharts.com

Notice in particular how many of these indices have more or less stabilized within various ranges since September even as the S&P 500 has zipped ever higher. The iShares 20+ Year Treasury Bond seems particularly reluctant to drive to lower prices (higher yields). The U.S. dollar index has spent a lot of the year meandering. Gold (GLD) is at the other end of this chart as it has dropped back down to its lows of the year. I am guessing early 2014 will deliver some major and important breakouts/breakdowns as tapering further unfolds. These inflection points may also bring fresh changes to the ways in which the Australian dollar trades in the coming year. Stay tuned (Stevens).

Be careful out there!

Disclosure: I am long TBT, SPHB, SPLV, GLD. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

Additional disclosure: I am also long SSO puts; long call and put options on EEM; in forex, I am net long USD and the Australian dollar.

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire