Many industrial companies are paying dividends. According to Portfolio123's database, 484 companies with a market cap greater than $100 million and price greater than $1.00 are classified as industrial. Among these companies, 266 companies are paying dividends, and 88 of them have a dividend yield greater than 2.0%.

I have searched for profitable industrial stocks that pay very rich dividends with a low payout ratio. Those stocks would also have to show a low debt.

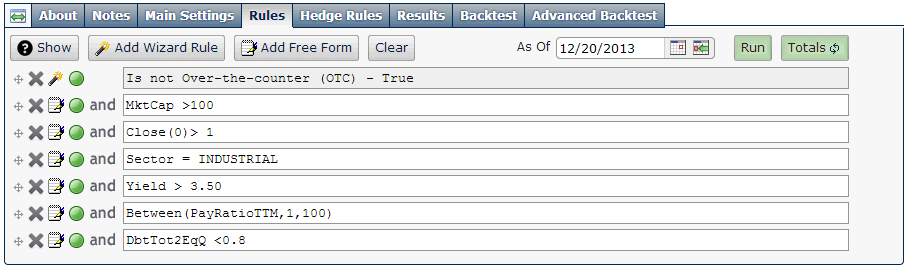

I used the Portfolio123's powerful screener to perform the search. The screen's formula requires all stocks to comply with all following demands:

- The stock does not trade over-the-counter [OTC].

- Market cap is greater than $100 million.

- Price is greater than 1.00.

- Sector is Industrial.

- Dividend yield is greater than 3.4%.

- The payout ratio is less than 100%.

- Total debt to equity is less than 0.80.

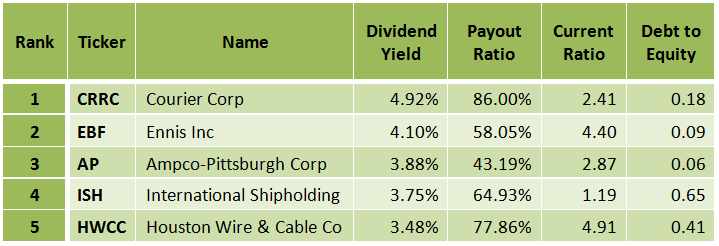

As a result, only five stocks came out, as shown in the charts below. In my opinion, these stocks can reward an investor a capital gain along with a high income. I recommend readers use this list of stocks as a basis for further research. All the data for this article were taken from Portfolio123 and finviz.com, on December 20, before the market open.

(click to enlarge)

(click to enlarge)

(click to enlarge)

Courier Corporation (CRRC)

Courier Corporation, together with its subsidiaries, prints, publishes, and sells books. It operates in two segments, Book Manufacturing and Publishing.

(click to enlarge)

Source: company presentation

Courier has a low debt (total debt to equity is only 0.18), and it has a trailing P/E of 17.44 and a forward P/E of 15.40. The price-to-sales ratio is very low at 0.70, and the price to book value is at 1.32. The forward annual dividend yield is very high at 4.92%, and the payout ratio is at 86%.

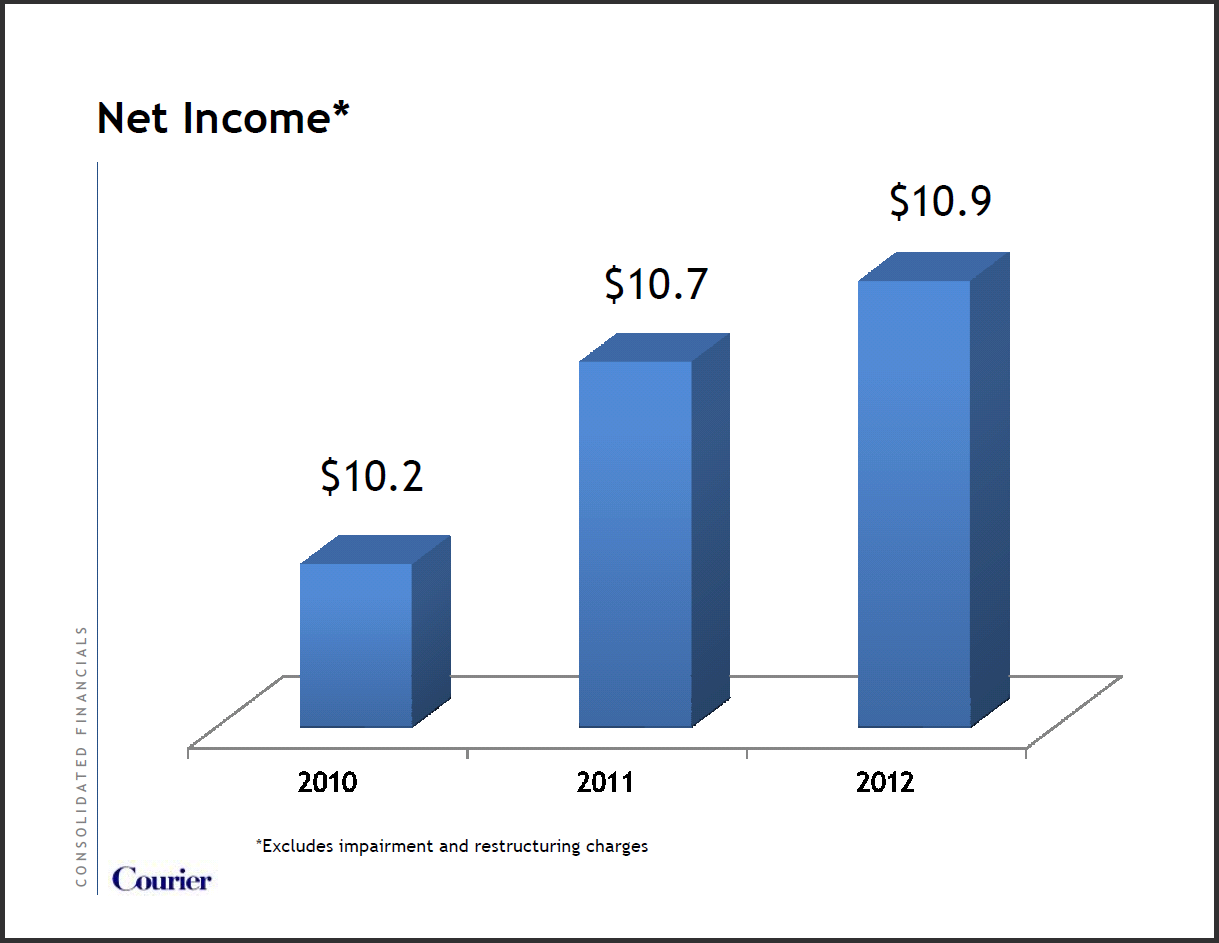

Courier has recorded strong EPS growth and moderate revenue growth, during the last year, the last three years and the last five years, as shown in the charts below.

(click to enlarge)

(click to enlarge)

Source: company presentation

Most of Courier's valuation parameters have been better than its industry median, sector median and the S&P 500 median, as shown in the tables below.

(click to enlarge)

Source: Portfolio123

On November 21, Courier reported its fourth-quarter fiscal 2013 financial results, which beat EPS expectations by $0.08. Fourth-quarter revenues in fiscal 2013 were $84 million, up 9% from $77 million in the fourth quarter of fiscal 2012. Net income in this year's fourth quarter was $6.8 million or $0.59 per diluted share, up from $5.7 million or $0.50 per diluted share in last year's fourth quarter.

Courier Corporation has recorded strong EPS growth, and considering the fact that the stock is in an uptrend, CRRC stock can move higher. Furthermore, the very rich dividend represents a gratifying income.

(click to enlarge)

Chart: finviz.com

Ennis Inc. (EBF)

Ennis, Inc., together with its subsidiaries, engages in the print and manufacture of business forms and other business products.

Ennis has a very low debt (total debt to equity is only 0.09) and it has a low trailing P/E of 14.12 and a very low forward P/E of 10.29. The PEG ratio is very low at 0.83, and the price-to-sales ratio is also very low at 0.85. The price to free cash flow for the trailing 12 months is very low at 11.58, and the average annual earnings growth estimates for the next five years is very high at 17%. The forward annual dividend yield is high at 4.10%, and the payout ratio is at 58%.

Ennis, Inc's stock valuation parameters have been much better than its industry median, sector median and the S&P 500 median, as shown in the table below.

(click to enlarge)

Ennis Inc. will report its next quarterly financial results on December 23. EBF is expected to post a profit of $0.40 a share, a $0.16 better than the company's actual earnings for the same quarter a year ago.

On September 23, Ennis reported its latest quarterly financial results.

Highlights for the quarter include:

- Consolidated gross profit margin increased 260 basis points for the quarter and 440 basis points for the period.

- Apparel gross profit margin increased 870 basis points for the quarter and 1,110 basis points for the period.

- Diluted EPS increased 31.0% to $0.38 per share for the quarter and 59.1% to $0.70 per share for the period.

In the report, Keith Walters, Chairman, Chief Executive Officer and President, commented by stating:

Overall we are pleased with our results for the quarter. Our apparel results continued to improve on both a sequential and comparative basis, as lower input costs of manufacturing and raw materials are favorably impacting their operational results. We realized a 270 basis point sequential margin improvement last quarter and a 280 basis point sequential margin improvement this quarter in our apparel margins. We would expect our apparel margin to continue to improve as our operational efficiencies improve as production levels increase. While the overall apparel market continues to be challenging, both from a pricing and volume perspective, we are seeing some pricing stability in the marketplace. Our print margin continues to remain healthy improving 30 basis points sequentially and 60 basis points for the period, as we continue to integrate acquisitions. We feel positive about the quarter and the remainder of the year.

Ennis, Inc. has compelling valuation metrics, and considering its strong earnings growth prospects, EBF stock still has room to go up. Furthermore, the very rich dividend represents a gratifying income.

(click to enlarge)

Chart: finviz.com

Ampco-Pittsburgh Corp. (AP)

Ampco-Pittsburgh Corporation, together with its subsidiaries, engages in manufacturing and selling custom designed engineering products in the United States and internationally.

Ampco-Pittsburgh has a very low debt (total debt to equity is only 0.06), and it has a very low trailing P/E of 11.18. The price-to-sales ratio is very low at 0.68, and the price to free cash flow for the trailing 12 months is also very low at 9.52. The price-to-cash ratio is very low at 2.08, and the price to book value is also very low at 0.93. The forward annual dividend yield is high at 3.88%, and the payout ratio is at 43.2%.

The AP stock price is 0.24% above its 20-day simple moving average, 2.25% above its 50-day simple moving average and 1.93% above its 200-day simple moving average. That indicates a short-term, a mid-term and a long-term uptrend.

On October 28, Ampco-Pittsburgh reported its third-quarter financial results. The company reported sales for the three and nine months ended September 30, 2013 of $64,433,000 and $203,995,000, respectively, against $72,190,000 and $215,751,000 for the comparable prior year periods. Income from operations approximated $20,777,000 and $24,879,000 for the three and nine months ended September 30, 2013, respectively, and includes a pre-tax credit of approximately $16,340,000, representing estimated additional insurance recoveries through 2022 for asbestos liabilities on account of insurance coverage settlement agreements entered into during the quarter. Income from operations for the three and nine months ended September 30, 2012 equaled $3,748,000 and $10,793,000, respectively.

Ampco-Pittsburgh has cheap valuation metrics, and considering the fact that the stock is in an uptrend and is trading below book value, AP stock still has room to go up. Furthermore, the rich dividend represents a nice income.

(click to enlarge)

Chart: finviz.com

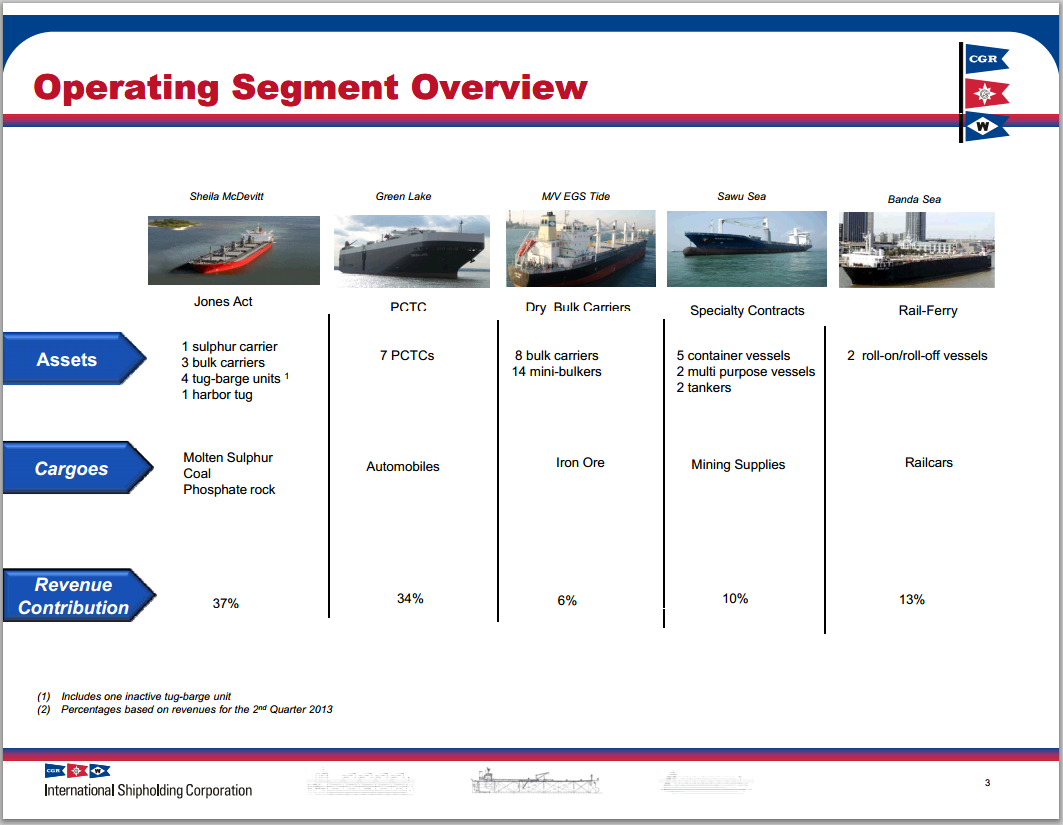

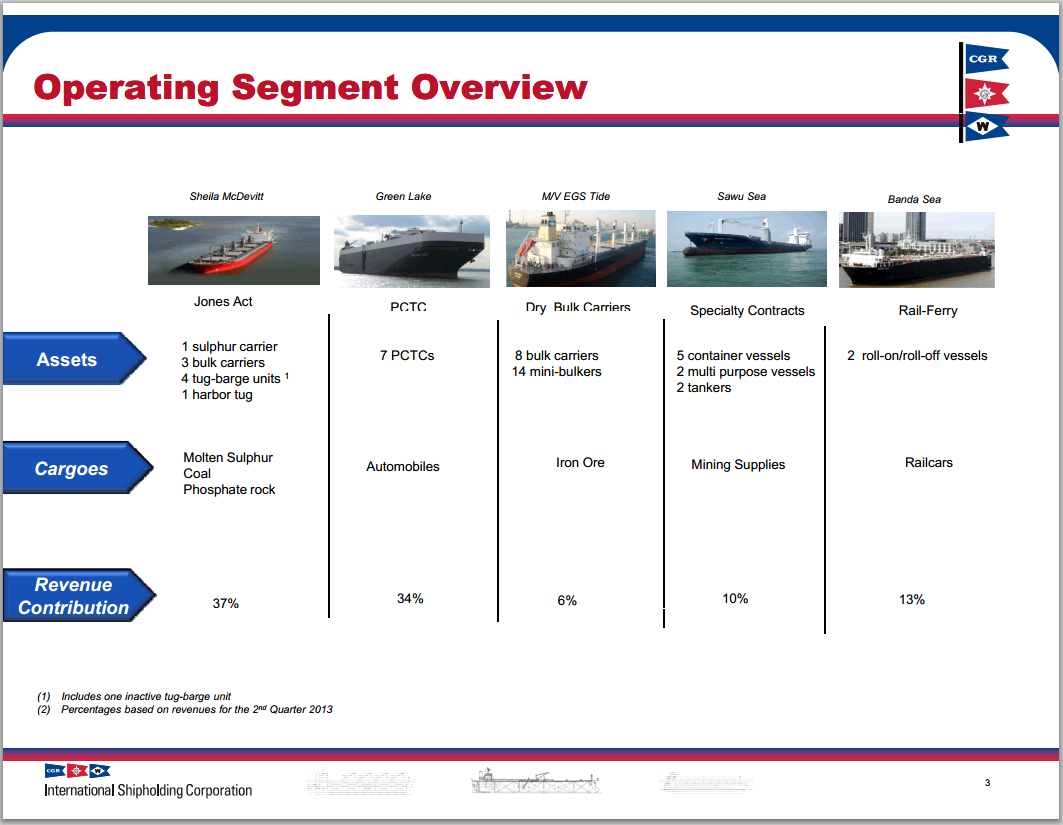

International Shipholding Corp. (ISH)

International Shipholding Corporation provides maritime transportation services to commercial and governmental customers primarily under the medium to long-term time charters or contracts of affreightment in the United States and internationally.

(click to enlarge)

(click to enlarge)

Source: company presentation

International Shipholding has a trailing P/E of 17.64 and a forward P/E of 19.23. The price-to-sales ratio is very low at 0.66, and the price to book value is also very low at 0.61. The forward annual dividend yield is quite high at 3.75%, and the payout ratio is at 64.9%

Analysts recommend the stock. Among the two analysts covering the stock, one rates it as a strong buy, and one rates it as a buy.

On October 30, International Shipholding reported its third-quarter financial results. EPS came in at $0.04 a $0.22 below expectations.

Third-Quarter 2013 Highlights

- Reported adjusted net income of $1.4 million for the three months ended September 30, 2013 excluding non-recurring charges of $3.6 million

- Completed a refinancing of its U.S. Flag fleet debt facilities, with a $45 million term loan and increasing its line of credit from $30 million up to $50 million. The new Facility also adds an accordion feature for up to an additional $50 million Facility

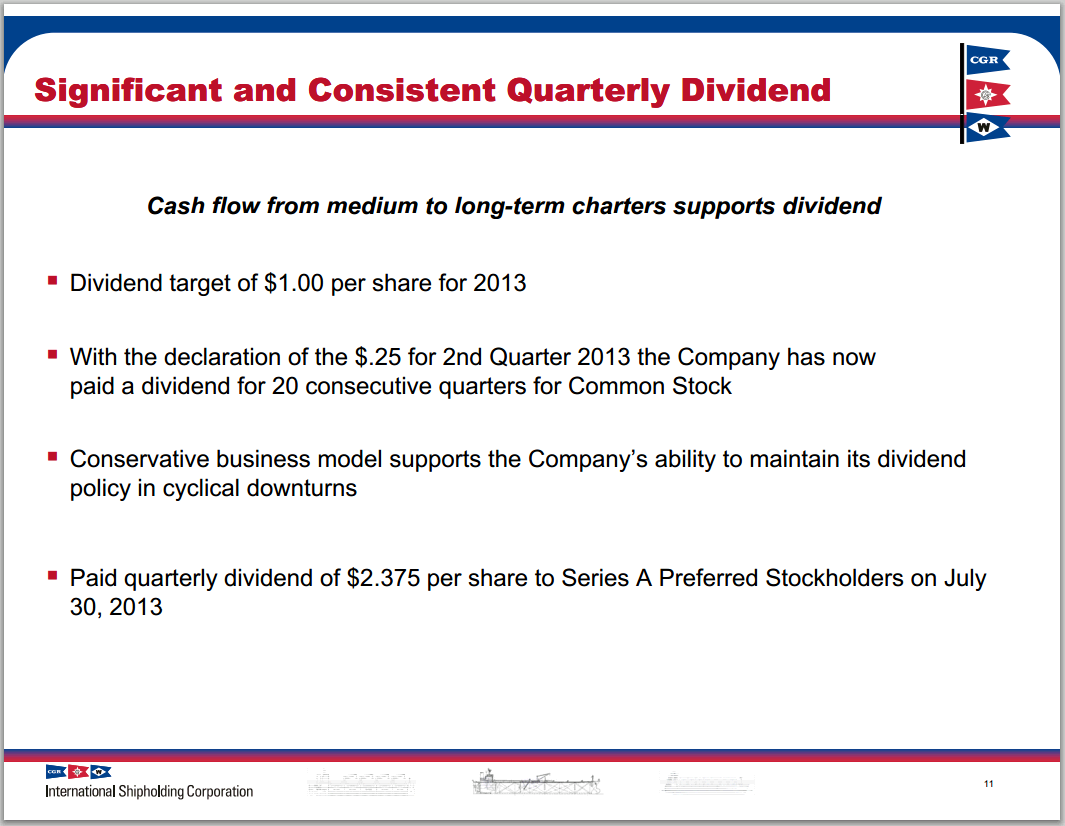

- Declared a third quarter dividend of $0.25 per share of common stock payable on December 3, 2013 to shareholders of record as of November 15, 2013

- Paid a $2.375 per share and $2.25 per share dividend on its Series A and Series B Preferred Stock, respectively, on October 30, 2013

The chart below, which was taken from the company presentation, emphasizes the significant and consistent quarterly dividend.

(click to enlarge)

International Shipholding has good valuation metrics and considering the stock is trading way below book value, ISH stock still has room to go up. Furthermore, the rich dividend represents a nice income.

Risks to the expected capital gain and to the dividend payment include; a downturn in the U.S. economy and a decline in sea freight rates.

(click to enlarge)

Chart: finviz.com

Houston Wire & Cable Company (HWCC)

Houston Wire & Cable Company, through its subsidiaries, provides wire and cable, hardware, and related services in the United States.

(click to enlarge)

Source: company presentation

Houston Wire & Cable Company has a low debt (total debt to equity is 0.41), and it has a trailing P/E of 24.80 and a very low forward P/E of 13.04. The PEG ratio is very low at 0.98, and the average annual earnings growth estimates for the next five years is quite high at 15%. The price to free cash flow for the trailing 12 months is very low at 11.39, and the price-to-sales ratio is also very low at 0.57. The forward annual dividend yield is quite high at 3.48%, and the payout ratio is at 77.9%. The annual rate of dividend growth over the past three years was at 5.59% and over the past five years was at 3.93%.

Houston Wire & Cable Company has recorded strong revenue and EPS growth during the last three years, as shown in the table below.

The company is penetrating to target markets, as shown in the chart below.

(click to enlarge)

Source: company presentation

On November 12, Houston Wire & Cable reported its third-quarter results, which missed EPS expectations by $0.03 and missed on revenues.

Third-Quarter 2013 Highlights

- Sales of $95.2 million

- Operating cash flow of $4.2 million

- Net loss of $3.2 million

- Adjusted net income of $3.5 million excluding impairment charge relating to the Southern Wire division

- Adjusted diluted EPS of $0.20 per share

- Debt decreased to $44.5 million, lowest level since Q1 2010

- Declared a dividend of $0.11 per share

Although Houston Wire & Cable missed Wall Street's expectations in its latest quarter report, the company has recorded revenue, EPS and dividend growth, and considering its compelling valuation metrics and its strong earnings growth prospects, HWCC stock can move higher. Furthermore, the rich dividend represents a nice income.

Risks to the expected capital gain and to the dividend payment include; a downturn in the U.S. economy, and shortage of new large capital projects.

(click to enlarge)

Chart: finviz.com

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire