2013 saw equities achieve their best overall annual return in over a decade. A majority of the rally was fueled by the expansion of multiples driven by the Federal Reserve's largesse and optimism that growth will accelerate in the year ahead. In addition, high momentum stocks with little earnings were a primary component of the market's outperformance. Highflyers like Netflix (NFLX), Tesla Motors (TSLA) and Amazon (AMZN) were big contributors to the market's rise.

(click to enlarge)

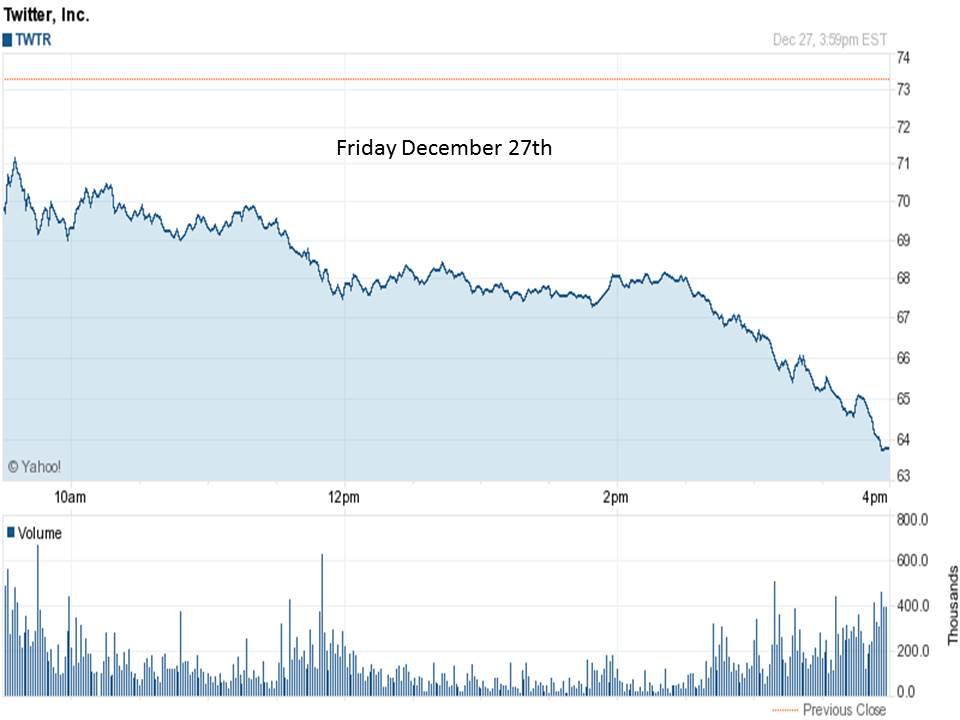

Neither factor is likely to continue in 2014. The Federal Reserve has announced it will start to withdraw liquidity from the market starting in January. Twitter (TWTR) gave a preview of what can happen to momentum stocks when sentiment shifts just a tiny bit on the stock. Twitter sold off 13% on Friday as Macquarie downgraded the shares to sell.

(click to enlarge)

Before Friday's sell-off Twitter has reached a $50B market capitalization at its recent highs. It also was selling at ~44x revenues with no prospect of earnings until FY2015. As I said earlier in the month, the stock is seriously overvalued and should be avoided. Barron's came out this weekend saying the shares still have farther to fall.

I believe 2014 will be a very different year for the stock market and investors. Multiple expansion should slow or stop completely as the Fed slowly withdraws the $85B a month it is pumping into the credit markets. This should leave the market's growth to be determined by earnings which should grow 5% to 10% next year according to the current consensus. This would be a solid return but not what investors have become accustomed to recently.

This should leave the market to be driven more by blue chips with consistently growing earnings, solid but not spectacular revenue gains and valuations below the overall market multiple. I think large cap tech can outperform the overall market in this type of environment. Here are three tech blue chips that I believe will turn in solid years in 2014 and should beat the overall market returns over the next twelve months.

Apple (AAPL) - It has been a tale of two halves for the Cupertino tech giant in 2013. In the first half of the year, the stock continued its decline from $700 a share it begun in September 2012. After reaching under $400 a share in late June, the stock has been on fire shooting up more than 40% to a current ~$560 a share.

I think this momentum will continue albeit at a lesser pace in 2014. The company's flagship iPad and iPhone franchises have successfully launched new versions of their iconic product lines. In addition, the company has signed NTT Docomo (DCM) and China Mobile (CHL) in recent months to carry the new iPhones. This gives Apple access to over 800mm new subscribers which should be a huge catalyst to growth in the coming year.

Consensus has the company printing ~8% sales and ~10% earnings increases in FY2014. I think these are conservative estimates that yet to factor in the full impacts of the new distribution deals in Asia. I also think investors can look forward to both a dividend increase and a rise in the company's stock buyback authorization in 2014. The company has an over $140B cash hoard that easily could enable both moves. The stock is still cheap at 11.7x FY2014's consensus earnings and also pays 2.2% dividend yield.

Microsoft (MSFT) - The big question around Mr. Softie as we head into the New Year is who its new leader will be in 2014. Whoever it is, he/she will have a lot to work with. Starting with the company's over $70B in net cash and marketable securities on the books. Capital allocation decisions to increase its dividend yet again and up the stock repurchase program will be welcomed by the market.

Microsoft has two web services (Azure and Office 365) businesses that each already has over $1B in annual sales and are growing rapidly. The company also recently launched its first Xbox console in seven years and it is selling extremely well. Even its new Surface tablets are a welcome improvement over its predecessors.

A new CEO might decide to spin off its search and non-core product lines in 2014 which activists will be happy to see. Revenues should grow in the 6% to 8% range annually over the next year or two. MSFT sells for less than 13x forward earnings (Just over 10x if you equate for net cash), a discount to the overall market multiple and also yields 3%.

Qualcomm (QCOM) - This mobile "arms merchant" was a hidden winner in Apple's recent distribution deals with China Mobile and NTT Docomo as it commits both carriers to continue to accelerate their efforts to expand their 4G networks which should boost demand for Qualcomm's product lines.

Qualcomm supplies Apple and all the major OEMs so it should be a long-term winner as long as mobile continues to grow at an impressive rate. As a result of the recent deals, consensus earnings estimates for both FY2014 and FY2015 have moved up nicely over the past three months.

Revenue growth is projected to be in the 8% to 10% annually over the next two fiscal years. QCOM sells for a little over 13x forward earnings, a discount to its five year average (16.8). The shares yield almost two percent (1.9%) as well. S&P has its highest rating "Strong Buy" on the shares as well as a $90 a share price target on the stock, ~25% above its current price level.

None of these selections is liable to set the world on fire in 2014. However, they should provide 10% to 20% capital appreciation in the New Year with 2% to 3% dividend yields thrown in to boot. I look for all three to outperform the more subdued market pundits are projecting for the coming twelve months.

Disclosure: I am long AAPL, MSFT, QCOM. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire