For investors looking for a tech company with strong fundamentals that is currently trading at a discount, Cisco Systems (CSCO) is a company worth further investigation.

Cisco Systems, Inc., designs, manufactures and sells Internet Protocol based networking and other products related to the communications and information technology industry and provides services associated with these products and their use.

In the section below, I will analyze aspects of Cisco's past performance. From this evaluation, we will be able to see how Cisco has fared over the past four years regarding their profitability, debt and capital, and operating efficiency. Based on this information, we will look for strengths and weaknesses in the company's fundamentals. This should give us an understanding of how the company has fared over the past few years and will give us an idea of what to expect in the future.

Profitability

Profitability is a class of financial metrics used to assess a business's ability to generate earnings compared with expenses and other relevant costs incurred during a specific period of time. In this section, we will look at four tests of profitability. They are: net income, operating cash flow, return on assets and quality of earnings. From these four metrics, we will establish if the company is making money and gauge the quality of the reported profits.

- Net income 2011 = $6.490 billion

- Net income 2012 = $8.041 billion

- Net income 2013 = $9.983 billion

- Net income 2014 TTM = $9.887 billion

Over the past three years, Cisco's net profits have increased from $6.490 billion in 2011, to $9.887 billion in 2014 TTM, which represents a 52.34% increase.

- Operating income 2011 = $7.674 billion

- Operating income 2012 = $10.065 billion

- Operating income 2013 = $11.196 billion

- Operating income 2014 TTM = $11.000 billion

Operating income is the cash generated from the operations of a company, generally defined as revenue less all operating expenses, but calculated through a series of adjustments to net income.

Over the past three years, Cisco's operating income has increased from $7.674 billion to $11.000 billion in 2014 TTM. This represents an increase of 43.34%.

ROA - Return On Assets = Net Income/Total Assets

ROA is an indicator of how profitable a company is relative to its total assets. ROA gives an idea as to how efficient management is at using its assets to generate earnings. Calculated by dividing a company's net income by its total assets, ROA is displayed as a percentage. Sometimes this is referred to as "return on investment."

Net income growth

- Net income 2011 = $6.490 billion

- Net income 2012 = $8.041 billion

- Net income 2013 = $9.983 billion

- Net income 2014 TTM = $9.887 billion

Total asset growth

- Total assets 2011 = $87.095 billion.

- Total assets 2012 = $91.759 billion.

- Total assets 2013 = $101.191 billion.

- Total assets 2014 TTM = $100.741 billion.

ROA - Return on assets

- Return on assets 2010 = 7.45%.

- Return on assets 2011 = 8.76%

- Return on assets 2012 = 9.87%.

- Return on assets 2013 TTM = 9.81%.

Over the past three years, Cisco's ROA has increased from 7.45% in 2010 to 9.81% in 2014 TTM. This indicates that the company is making slightly more on its assets than it did in a few years ago.

Debt And Capital

The Debt and Capital section establishes if the company is sinking into debt or digging its way out. It will also determine if the company is growing organically or raising cash by selling off stock.

Total Liabilities To Total Assets, Or TL/A ratio

TL/A ratio is a metric used to measure a company's financial risk by determining how much of the company's assets have been financed by debt.

Total assets

- Total assets 2011 = $87.095 billion.

- Total assets 2012 = $91.759 billion.

- Total assets 2013 = $101.191 billion.

- Total assets 2014 TTM = $100.741 billion.

- Equals an increase of $13.646 billion

Total liabilities

- Total liabilities 2011 = $39.869 billion

- Total liabilities 2012 = $40.473 billion

- Total liabilities 2013 = $42.071 billion

- Total liabilities 2014 TTM = $41.844 billion

- Equals an increase of $1.975 billion

Over the past three years, Cisco's total assets have increased by $13.646 billion, while the total liabilities have increased by $1.975 billion. This indicates that the company's assets have significantly outpaced the increase in liabilities thus adding shareholder value.

CSCO Total Assets (Quarterly) data by YCharts

Working Capital

Working Capital is a general and quick measure of liquidity of a firm. It represents the margin of safety or cushion available to the creditors. It is an index of the firm's financial stability. It is also an index of technical solvency and an index of the strength of working capital.

Current Ratio = Current assets / Current liabilities

Current assets

- Current assets 2011 = $57.231 billion

- Current assets 2012 = $61.933 billion

- Current assets 2013 = $65.521 billion

- Current assets 2014 TTM = $62.796 billion

Current liabilities

- Current liabilities 2011 = $17.506 billion

- Current liabilities 2012 = $17.731 billion

- Current liabilities 2013 = $22.192 billion

- Current liabilities 2014 TTM = $21.728 billion

- Current Ratio

- Current ratio 2010 = 3.27

- Current ratio 2011 = 3.49

- Current ratio 2012 = 2.95

- Current ratio 2013 = 2.89

Over the past three years, Cisco's current ratio has decreased. As the current ratio is currently well above 1, this indicates that Cisco would be able to pay off its obligations if they came due at this point. If the ratio were to drop closer to 1.00 that would raise some concerns.

Common Shares Outstanding

- 2011 shares outstanding = 5.563 billion

- 2012 shares outstanding = 5.404 billion.

- 2013 shares outstanding = 5.380 billion

- Current shares outstanding = 5.430 billion

Over the past three years, the number of company shares has remained relatively flat. The company shares have dropped from 5.563 billion to 5.430 billion a decrease of 2.4%

Operating Efficiency

Operating Efficiency is a market condition that exists when participants can execute transactions and receive services at a price that equates fairly to the actual costs required to provide them. An operationally efficient market allows investors to make transactions that move the market further toward the overall goal of prudent capital allocation without being chiseled down by excessive frictional costs, which would reduce the risk/reward profile of the transaction.

Gross Margin: Gross Income/Sales

The Gross Profit Margin is a measurement of a company's manufacturing and distribution efficiency during the production process. The gross profit tells an investor the percentage of revenue/sales left after subtracting the cost of goods sold. A company that boasts a higher gross profit margin than its competitors and industry is more efficient. Investors tend to pay more for businesses that have higher efficiency ratings than their competitors, as these businesses should be able to make a decent profit as long as overhead costs are controlled (overhead refers to rent, utilities, etc.).

- Gross margin 2011 = $26.536 billion / $43.218 billion = 61.40%.

- Gross margin 2012 = $28.209 billion / $46.061 billion = 61.24%.

- Gross margin 2013 = $29.440 billion / $48.607 billion = 60.57%.

- Gross margin 2014 TTM = $29.608 billion / $48.816 billion = 60.65%.

Over the past three years, Cisco's gross margin has slightly decreased. The ratio has decreased from 61.40% in 2011 to 60.65% in 2014 TTM.

Asset Turnover

The formula for the asset turnover ratio evaluates how well a company is utilizing its assets to produce revenue. The numerator of the asset turnover ratio formula shows revenue found on a company's income statement and the denominator shows total assets, which are found on a company's balance sheet. Total assets should be averaged over the period of time that is being evaluated.

Revenue growth

- Revenue 2010 = $43.218 billion

- Revenue 2011 = $46.061 billion

- Revenue 2012 = $48.607 billion

- Revenue 2013 = $48.816 billion

- Equals an increase of 12.95%

Total Asset growth

- Total assets 2011 = $87.095 billion.

- Total assets 2012 = $91.759 billion.

- Total assets 2013 = $101.191 billion.

- Total assets 2014 TTM = $100.741 billion

- Equals an increase of 15.67%.

Over the three years the revenue growth has increased by 12.95% while the assets have increased by 15.67%. This is an indication that the company from a percentage point of view has been less efficient at generating revenue with its assets.

Based on the information above we can see that Cisco Systems fundamentally has had a strong few years. Some of the strengths include the TL/A ratio which indicates that Cisco assets are increasing much faster than the company's liabilities. Another strong point is that the ROA is increasing indicating an increase in shareholder value. Over the past three years the revenue has increased by 12.95% while the net income has increased by 52.34% indicating that Cisco is becoming more efficient. A blemish that the analysis reveals is: A decrease in the gross margin. Over the past three years the gross margin has fallen from 61.40% to 60.65% but this is only a minor flaw as the percentage is slight. From a fundamental point of view Cisco systems is displaying strong results.

Headwinds and Downtrend

Because Cisco is facing many headwinds the sentiment for the stock has turned negative in August. Some of the reasons for the negative sentiment is they reported are having issues entering emerging markets, they are facing conservative customer spending and stalling growth in its core business of network equipment.

All of these issues have resulted in the company has reducing its medium term forecast revenue rate to a range of 3-6%, down from 5%-7% as reported earlier this year.

Even though there is much negative sentiment Cisco has bullish arguments moving forward as well. Recently they were upgraded by S&P from "AA-" from "A+" and recently Cisco reported a share buyback program.

Because of its strong fundamentals, In December 2013, Cisco Systems was raised by S&P up to "AA-" from "A+". S&P forecasts continued strong EBITDA and cash flow generation despite challenging market conditions. They also stated "Cisco is likely to expand its shareholder return and acquisition strategies over the intermediate term."

On Nov. 13th Cisco announced that its board of directors authorized up to $15 billion in additional repurchases of its common stock. Cisco's board had previously authorized up to $82 billion in stock repurchases. There is no fixed termination date for the repurchase program. The remaining authorized amount for stock repurchases under this program, including the additional authorization, is approximately $16.1 billion.

Valuations

In the section below, I will use a couple of different methods to find a valuation of the stock price. In this section, I will use the Discounted Cash Flow valuation model and forward P/E ratios to estimate the current value of each share.

I believe using the Discounted Cash Flow valuation model for Cisco Systems to be fair because DCF analysis can help one see where the company's value is coming from and one can generate an opinion based on that.

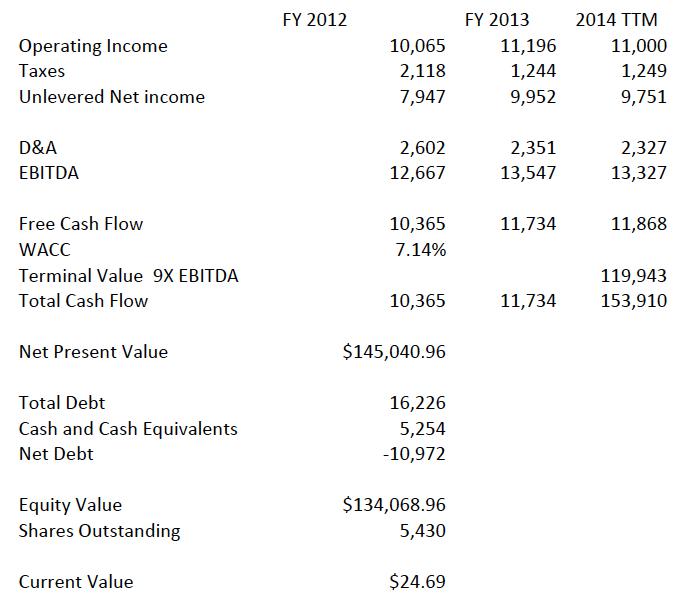

(click to enlarge)

Even though there are variations in calculating this formula, this model is based off of a terminal value of $119.943B and a WACC of 7.14%. The terminal value $119.943B is based off of the company trading at 9X EBITDA. At this point in the market, I believe 9x EBITDA to be conservative as forward P/E ratio is estimated at 10.58. The EBITDA should trade at a discount to this value. Using the valuations above, I have concluded Cisco's current value to be $24.69 per share.

Looking forward to 2014, I will use Cisco's forward P/E ratios with estimated earnings to find the value. Currently, Google has a forward P/E of 10.58 and FY 2016 earnings projected at $2.19. These two metrics lead to a target price of $23.17.

As of December 29th, Cisco's stock was trading at $22.02 - Using the Discount Cash Flow Formula, this indicates the stock is currently undervalued by 12.13%. Looking forward to 2014, If I calculate a valuation using a forward P/E of 10.58 ratios this indicates a valuation $23.17 or a discount of 5.22%.

Strategy

Based on the chart listed above I would wait for the down-trend to stop before entering a position or adding to a position. From this point If the stock breaks the $20.00 support range this would be a sell signal for me. Currently, I believe there is upside to equity markets as major world economies are either recovering or on the verge of recovering. As interest rates continue to remain near zero this should favor equities.

Conclusion

Currently, Cisco's stock is in a strong downtrend. Over the past few months the stock price has not participated in the bull market. Even though the current fundamental suggest strength, I would wait for this trend to stop. If the stock drops below $20.00 this would constitute a sell signal. As estimates indicate that Cisco will produce an EPS of $2.19 in 2016 combine that with a forward P/E ratio of 10.58 this produces a 2014 target of $23.17. At current levels using the Discount Cash Flow Formula, I believe the stock is currently undervalued by 12.13% but I would wait for the downtrend to stop before considering a position in Cisco Systems.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire