LinkedIn Corp (LNKD) operates a social networking website used for professional networking. It is a professional network with more than 225 million members in over 200 countries. In the social networking industry no company currently capitalizes on its users more effectively than LinkedIn. With an attractive business model and a loyal customer base thanks to its popularity and potential advantages over conventional job hunting this wide-moat firm is one of the few social networking companies that genuinely hold a long-term defensible position.

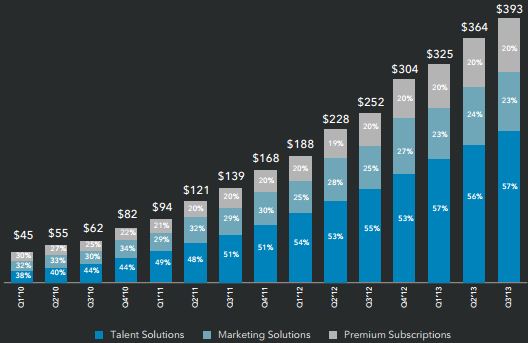

To begin with, we will have a look at the core driver of a company: revenue. During the last quarter, LinkedIn reported revenues of $393 million increasing 56% since the third quarter of 2012! LinkedIn operates in three segments: talent, marketing and premium subscriptions. While the marketing and premium subscription segment generates revenue from posting ads and receiving subscriptions from members to access premium services, the talent segment, 57% of the company (in terms of revenue), derives its income from allowing recruiters to use LinkedIn's database to locate potential job candidates.

Talent Solutions

Revenue from Talent Solutions products totaled $224.7 million reflecting an increase of 62% compared to the third quarter of 2012. Talent solutions' revenue represented 57% of the total revenue this quarter compared to 55% in the third quarter of 2012. The graph below shows that the talent segment has been increasing its share over the past several quarters.

(click to enlarge)

Expansion from enterprise customers is a key component for Talent solutions' growth. The expansion also supports the growth of job postings on LinkedIn. During the third quarter the number of open jobs accelerated and surpassed the 300,000 mark. Since 2010, LinkedIn has focused on increasing jobs through the field sales channel with enterprise customers representing nearly 90% of open jobs versus less than 50% three years ago. This trend expected to continue so we can expect more growth in the segment in the future.

Marketing Solutions

Revenue from marketing solutions' services totaled $88.5 million reflecting an increase of 38% compared to the third quarter of 2012. Marketing solutions' revenue represented 23% of total revenue in the third quarter of 2013 compared to 25% in the third quarter of 2012.

The growth is explained by LinkedIn's diversion from customer-focused activity and traditional display advertising formats towards sponsored updates. Moreover, mobile device usage is driving approximately 67% of the revenue of sponsored updates which is in turn driven by higher click-through rates on phones and tablets. The mobile trend will significantly boost LinkedIn's revenue in the ad business in 2014 after the company installs the infrastructure it will need to operate on a much larger scale.

Premium Solutions

Revenue from premium subscriptions' services totaled $79.8 million reflecting an increase of 61% compared to the third quarter of 2012. Premium subscriptions represented 20% of total revenue in the third quarters of 2013 and 2012.

I don't think this segment could potentially dominate the other segments. One reason is because the trend shown in the graph above reflects the declining share of total revenue of this segment. Secondly, even though the company is trying to retain more customers and renewals are at an all-time high this quarter with a churn rate of 50%, long term this cannot be a primary source of revenue because not many users want to pay to find a job.

Income and Reason Behind Losses

Despite the increasing sales momentum the company reported a net loss for the third quarter of $3.4 million compared to net income of $2.3 million in the third quarter of 2012. This resulted in the diluted GAAP EPS turning from positive $0.39 to negative at $0.03 during the third quarter of 2012.

The reason behind the company's reported losses is explained in its ongoing long-term tax optimization strategy. Currently, LinkedIn paid a 170% GAAP tax rate which is very high. When LinkedIn began scaling business globally in 2009 it put in place an international tax structure to optimize its long-term tax rate. In the short-term, this strategy will result in a higher tax impact until LinkedIn reaches profitable scale outside the US over the next few years. Secondly, since LinkedIn is growing its international revenue quarter by quarter (see graph below) we can expect LinkedIn to increase its profit levels enough to turn GAAP reported losses into profits. Therefore, if we exclude taxation this quarter, non GAAP income increased by more than 80% to $46.8 million at a tax rate of just 26%! This is only one side of LinkedIn's long term plans.

Now, let us look at the performance from the other side. The operating cash flows increased by 43% to $126 million this quarter. Free cash flow decreased by 20% to $43 million because it included CAPEX investment ($83 million) on LinkedIn's first self-managed data centre which it began testing in the third quarter. Otherwise, free cash were 133% higher than the previous quarter in 2012!

New Programs to Provide Future Competitive Edge

LinkedIn also recently launched two new mobile services "work with us" and "recruiter mobile". These services have simplified the search and connectivity for both job seekers and recruiters in a way like no other professional networking site has done before. Other highlights that will bring strong momentum for LinkedIn in the future are listed below:

- Membership has surpassed 259 million members as growth increased to 38% year-over-year and members engaged at record levels across desktop and mobile devices in the latest quarter. This is a good sign as the increasing user base confirms our belief in LinkedIn's popularity.

- LinkedIn launched University pages, its first initiative to create a resource for students bringing them to the website as potential clients. At present, there have been more than 1500 pages created in more than 60 countries.

- The company launched sponsored updates, LinkedIn's first mobile advertising service designed to deliver relevant content to members from marketers. According to Google this will be a success since mobile clicks are increasing and mobile platforms provide a good base for future revenue growth.

Additionally, LinkedIn launched several new mobile services that included a new iPad app and Intro for iPhone that transforms the mobile email experience. Also, a new Pulse app to deliver relevant news and insights to users was launched.

These new features will continue to keep users engaged and the added flexibility provided will encourage more sign ups in the future.

Technical Aspects

Another good thing is the fact that the company's five-year annualized growth rate is greater than 100%. Analysts forecasted a 106% EPS increase in 2012. Actual earnings growth turned out to be 154% in 2012. Expecting the same trend in 2013, they now believe the EPS will be $1.61 rather than the $1.28 previously forecast.

Final Verdict and the Truth about Social Networking Stocks

Even though the fundamentals lagged behind the industry figures with the return on equity being only 11% (less than the standard 17% investors should seek) and pre-tax profit margin were 11% this can be overlooked because sometimes fundamentals do not provide a clear picture of a company's standing. This is true for LinkedIn whose 3Q12 EPS rose 267% due to a sales growth of 81% on a yearly basis.

Conclusion

We can only wait for market optimism to decrease and bring a depressing short term effect on the price in order to get a quick gain on the stock. Nonetheless, LinkedIn is a wise choice as no rival holds a stronger edge in the industry. In fact, the market operates as such that only one player can rule or dominate. Others are wiped out as candidates on the less popular sites shift towards more popular offerings in order to keep up with the competition.

This shouldn't come as a surprise since we know the fate of social networking sites like Orkut and Hi5 that were taken over by Facebook. Similarly, LinkedIn is the leader in professional networking. However, we must remember the downside risk associated with networking websites. It doesn't take long for them to be taken over. It won't be a matter of years but instead weeks until we can expect prices to fall. For this reason, investors are warned to be cautious in retaining large blocks of social networking stock. Otherwise, LinkedIn is a good choice and I recommend buying the company's stocks.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire