Gold in 2013: well that was quite a year but you should have seen it coming.

Gold (GLD) never ceases to generate numerous, and sometimes spurious, headlines both in the good years and the bad years. The following article gives some interesting facts about what happened over the past year and winds up with a short lesson on why we the dramatic losses of 2013 should not have been a surprise.

Fact number 1 - with a loss for the year of just over 27% gold had its worst year in 32 years

You probably know that already, especially if you own gold. Actually, you are probably sick of hearing about it - but read on and you'll find some interesting points to consider.

It won't make you feel better to know that back in the year that Ronald Reagan became US President, Princess Di married someone called Charles and I was just beginning primary school, gold lost even more than over this past year, with a 33% loss. (It was 1981. by the way).

Fact number 2 - despite the dramatic loss, if you bought gold before 2010 you are still making a profit

Some investors probably forgot that gold can actually go down in price, given that it has not done so for the last twelve years. Here are the annual returns since the run of 12 consecutive gains began, back in 2001.

(click to enlarge)

If you bought gold anytime before the beginning of 2010, you would still be sitting on a nice profit despite the dramatic loss over the last 12 months.

In fact if you bought a nice lump sum at the beginning of this bull run on 1st Jan 2001 and went to sleep only to wake up on 1st Jan 2014, and someone told you that your gold investment had brought in an equivalent annual return of 12%, you'd probably pocket it and say thank you very much with a smile on your face.

Even someone buying as recently as 1st Jan 2009 would still be looking at an annual equivalent return of almost 7.0%. So this fall in gold price has only hit hard those investors who have piled in over the last few years.

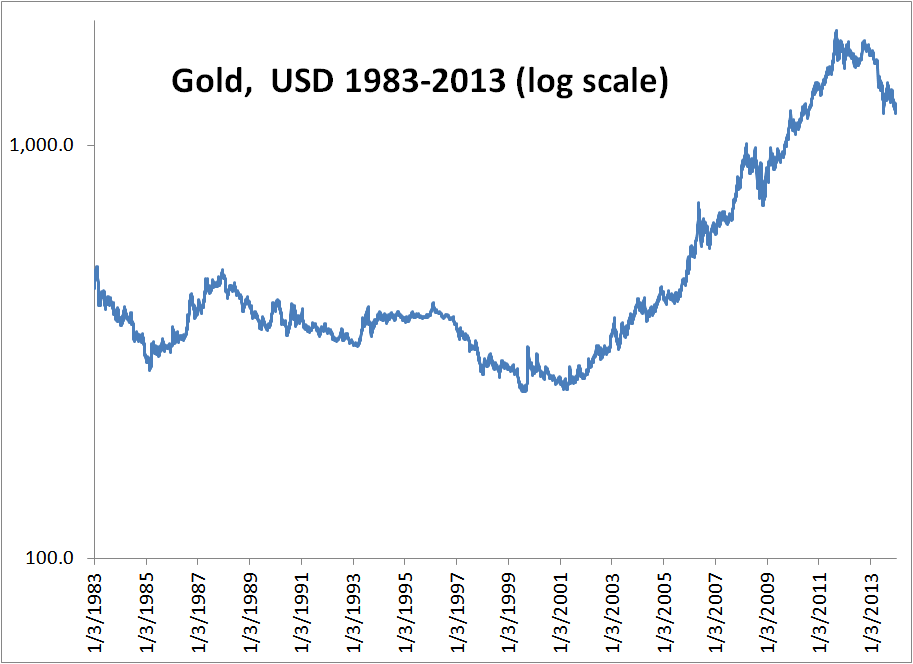

Perspective is always useful, and the following graph shows the long term price of gold on a logarithmic scale. (For those unfamiliar with the concept, a $10 price move when gold is worth $100 is far more significant than a $10 move when gold is worth $1,000. A logarithmic scale corrects for this and shows proportional changes as being equal, as opposed to a regular graph which shows absolute changes as being equal).

(click to enlarge)

Fact number 3 - with a volatility of 21.6% in 2013 gold was only slightly more volatile than its long term average

Any investor buying an asset should be aware of two characteristics that define the main feature of that asset - returns and risk. The investment world normally measures the price risk of an asset using the concept of volatility.

We have heard a lot about the returns of gold over 2013, but not very much about the volatility or riskiness of gold. Well, perhaps surprisingly, the volatility of gold in 2013 at 21.6% was not too far from the long term average over the last thirty years, of almost 16%.

The following chart shows the annual volatility of gold over the last thirty years.

(click to enlarge)

As we see in the chart, gold's volatility spiked up in 2008 (which asset class's didn't?) but the latest year's volatility, whilst higher than the sedate years of the 1990s, is not too far removed from that seen over a number of recent years.

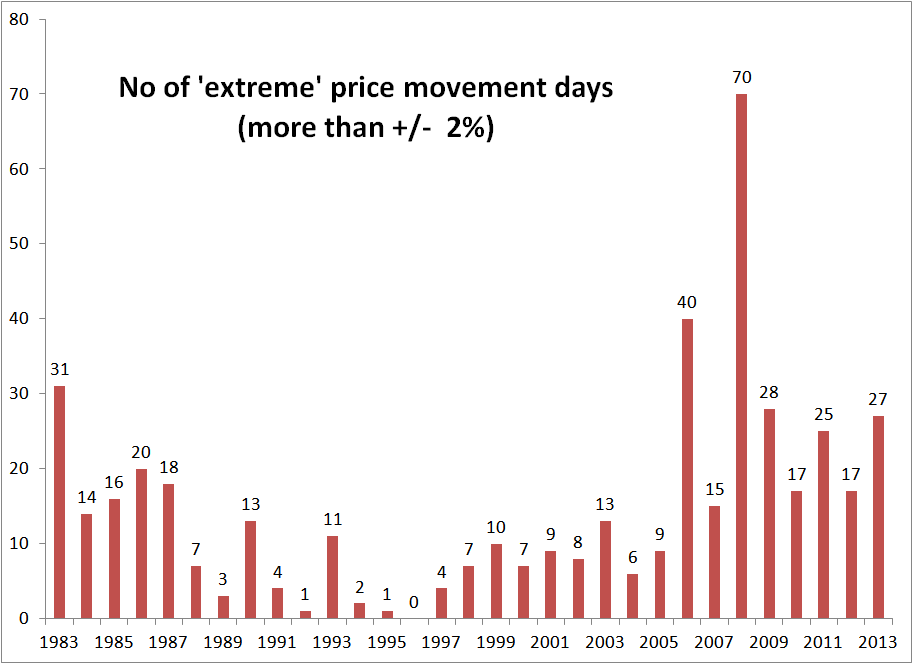

Another way of looking at volatility, perhaps in easier terms for the less technical investor, is to see how many days were 'extreme' price movement days in the sense that prices moved over a certain threshold.

The following graph which shows the number of trading days in which gold moved than 2% either up or down in one day, when comparing the closing prices, illustrates a similar story.

(click to enlarge)

Fact number 4 - if you knew fact number 3, you should have expected fact number 1.

(Or in plainer English - an investor who knows the riskiness of an asset should not be surprised by large losses of a certain magnitude from time to time).

Let me explain with a crash course in what volatility means, in simple layman terms. (Don't get deterred by the technical terms - I'm going to explain it very simply and clearly).

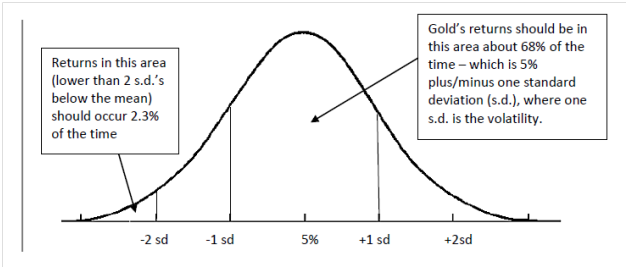

We'll take the case of gold to explain volatility and to explain my point. Gold, as I explained above, has a long term annual volatility of about 16%, based on the last thirty years. Over the same time period, the average annual return of gold has been about 5%.

When we talk about volatility in financial assets, the number refers to a percentage which is one standard deviation (I'll explain this very shortly) away from the mean. Under certain assumptions about how returns are distributed, we would expect the returns of an asset (in this case gold) to be plus or minus one standard deviation from the mean (average) return, approximately 68% of the time.

(When you hear volatility for any asset class, this means that returns will be within that distance from the average return on about two thirds of the time).

So for gold, with an annual return of 5% and a volatility of 16%, we would expect returns to be between -11% and 21% (i.e. 5% +/- 16%) for approximately 68% of the time.

(click to enlarge)

Similarly, again according to certain assumptions, returns should be in the region which is lower than 2 standard deviations below the average return, on just over 2% of occasions. This translates, for gold, into returns being worse than a loss of 27% (5% - 2*16%) or lower on just over 2% of the time - or in annual terms, about once every forty years.

So considering that this is the first time gold's returns have fallen in that area of the graph, for 32 years - once every 40 years is not too far off. And pretty much matches up with what the return and risk characteristics of gold are telling us.

The important point for investors is to remember that the 'volatility' of an asset is not a meaningless concept, and it is vital to understand what it means. Too often investors just focus on the returns of different assets - especially after over a decade of positive returns. But they forget that risk or volatility is just as an important feature.

You can't use it to predict when gold (or any other asset) is going to have a 'two standard deviation event', but the fact that it does every 40 years should not come as a surprise.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire