A year ago I started a comparison between the "Dogs of the Dow" portfolio and a portfolio of companies selected on the basis of my "PIC" criteria. Each portfolio contained 10 holdings which were to remain untouched for the year (although this becomes something of a bone of contention, as it turns out). I then expanded the comparison to include portfolios drawn from the S&P 500, one made up of "dogs" and the other made up of PICs. I would like to summarize what has amounted to an unusual year for the market by showing the final results of the two comparisons.

The Dow Jones Industrials

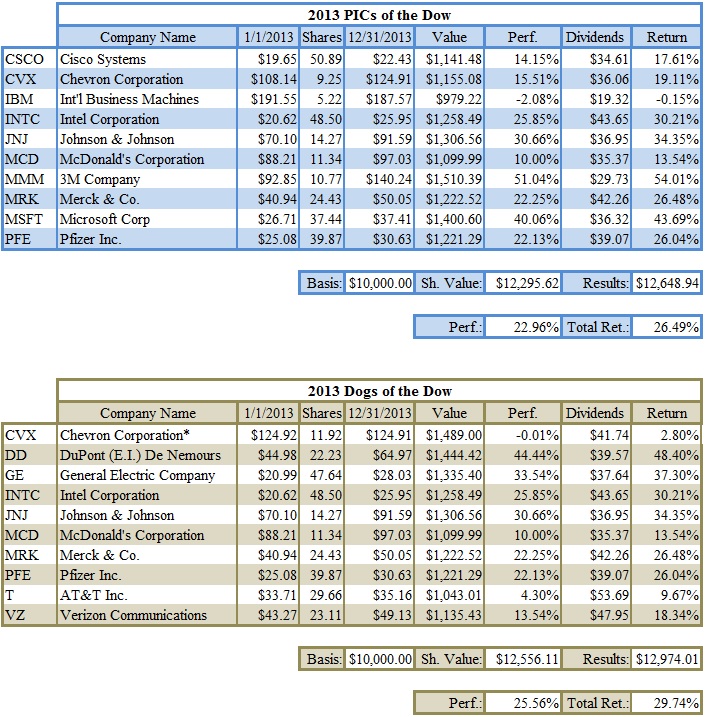

We get to discuss controversy right off the bat as we consider the following table summarizing the year's Dow comparison:

(click to enlarge)

The original Dog portfolio contained Hewlett-Packard Co. (HPQ) (aka, "HP") as one of the holdings. Unfortunately, on September 20, HP was dropped from the Dow's 30 industrials (along with Bank of America Corp. (BAC) and Alcoa Inc. (AA)).1 In response, I replaced HP with Chevron Corporation (CVX) which at the time had the highest dividend yield. My thinking was that, HP no longer being a Dow company, it was appropriate to replace it.2

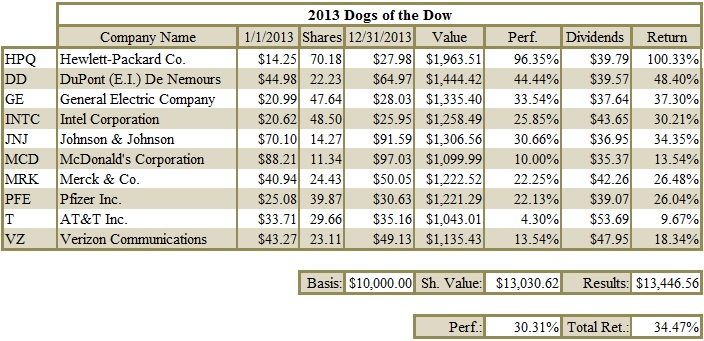

The decision-makers at Dow Jones might be kicking themselves about now, as HP significantly outperformed Chevron, increasing in value by more than 96%, while Chevron's performance for the year was approximately 15%, and - since its "induction" into the Dog portfolio - actually dropping by 0.01%. Had HP been kept in the Dog portfolio, the results would have looked like this:

(click to enlarge)

Those who held on to HP were amply rewarded for their loyalty. Wanting to be a purist about the whole thing (and seeing that HP was going to skew the Dogs way too high), I shifted to Chevron.

At least it made things a bit closer.

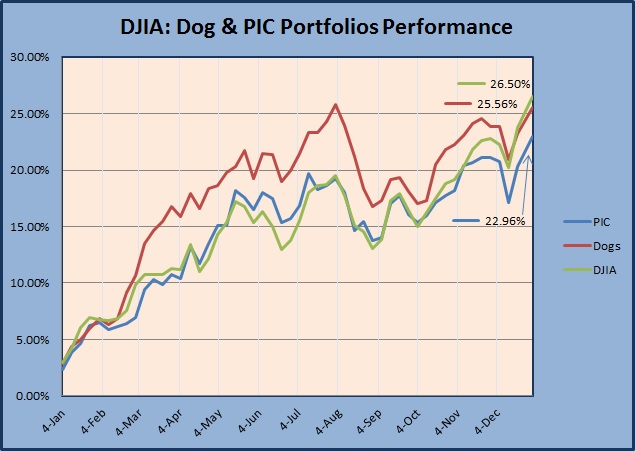

The following chart compares the performance of the two portfolios (without dividends) as compared to the performance of the DJIA as a whole:

(click to enlarge)

With Chevron added to the portfolio, the Dow actually outperformed the Dogs by 94 basis points. Both the Dow and the Dogs handily beat the PIC portfolio which lagged 260 basis points behind the Dogs.

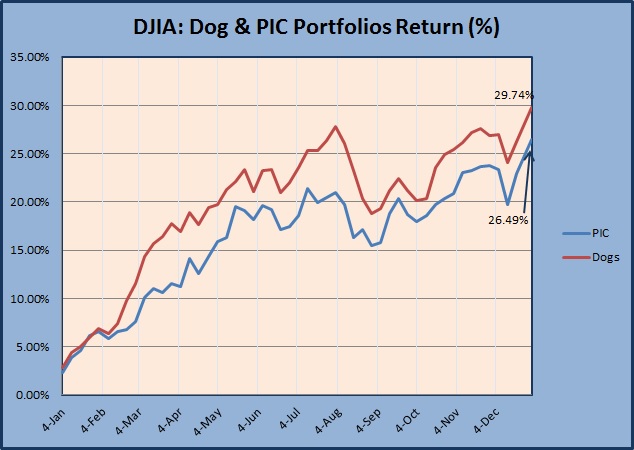

Adding dividends to the mixture, the Dogs and the PIC give us the following graph:

(click to enlarge)

A difference of 325 basis points counts as a significant loss, although I wouldn't object to having a portfolio that paid me 26% per year.

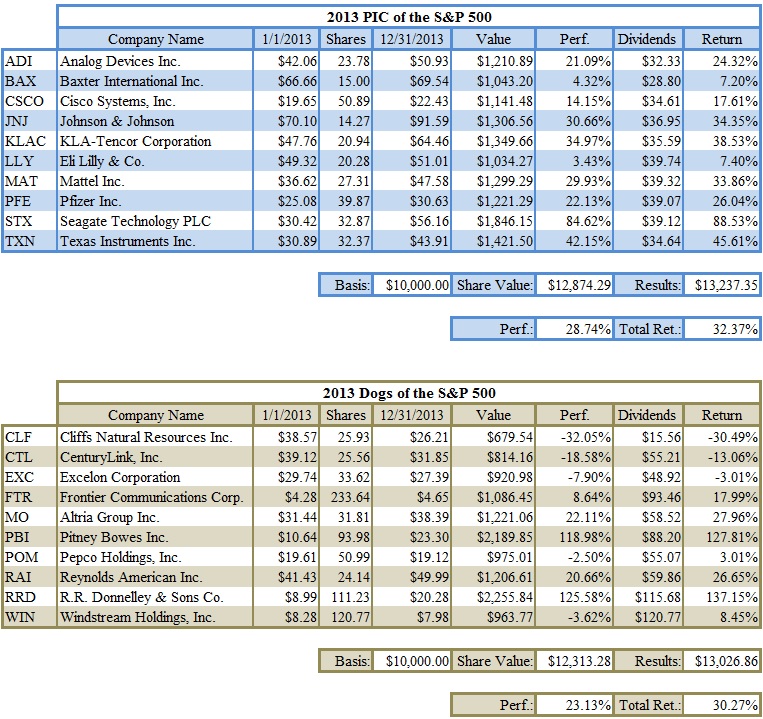

The S&P 500

The surge in the stock market after the government shutdown ended up pushing the S&P 500 over both portfolios in this comparison, and made the results between the Dog and PIC portfolios closer than had been the case for most of the year. The table below gives us a summary of the two portfolios:

(click to enlarge)

The Dog portfolio had five companies with negative performances - three of those even remaining negative after the addition of dividends. How did the portfolio manage a more-than-23% performance and 30% total return? Two of its holdings were bona fide two-baggers: Pitney Bowes Inc. (PBI) and R.R. Donnelley & Sons Co. (RRD).

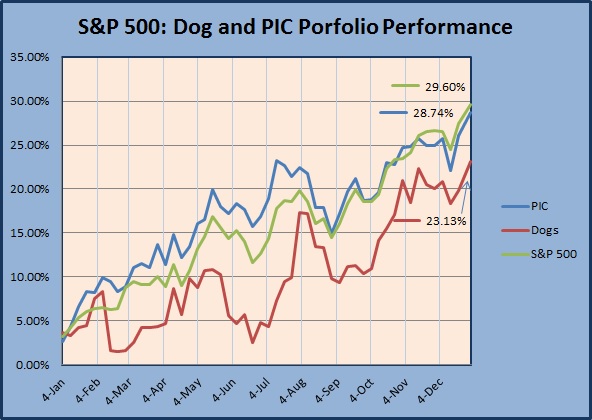

The following graph shows the performance of the two portfolios compared to the performance of the S&P 500 itself (again, without dividends factored in):

(click to enlarge)

There was never much doubt that the PIC portfolio was solidly outperforming the Dogs of the S&P, ending up 647 basis points ahead. Less certain was the "race" with the S&P 500 index. In the end, the last two months saw the S&P gain and hold on to a lead of 86 basis points, after trailing the PICs for most of the year.

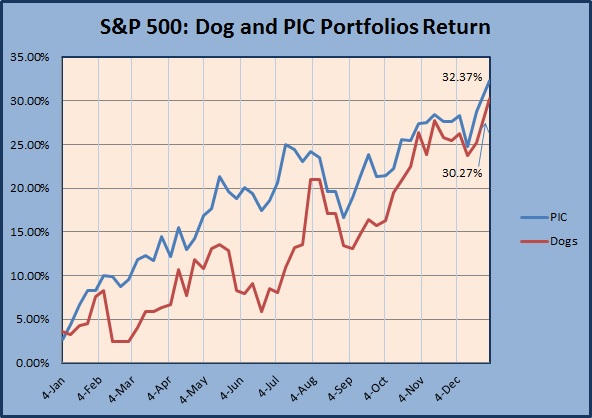

While the PIC portfolio maintained a substantial lead over the Dogs in terms of performance, something interesting happens when we factor in the dividends paid:

(click to enlarge)

Once we add dividends into the mix, what had been a 647-basis-point rout turns into a much narrower 210-basis-point win.

Reflections

All four of the portfolios considered above performed in keeping with their respective index; none of them performed exceptionally well, and none of them performed exceptionally poorly. A case can be made for saying that the Dogs of the S&P portfolio got lucky in having two two-baggers in what was otherwise a mediocre collection of holdings - but there is something to be said for the way the portfolio's dividends affected its total return, which has nothing to do with how Pitney Bowes or R.R. Donnelley performed.

The Dow Jones 30 Industrials is a collection of large, well-performing, companies selected on the basis of criteria that emphasize those qualities. It is, then, no great surprise that neither the Dog portfolio nor the PIC portfolio performed substantially better or worse than the DJIA (especially given the general fervor that seemed to grasp the markets).

The greater performance of the Dogs over the PICs is no doubt due to some extent by the fact that where there were differences between the two portfolios the Dogs were favored with companies that were low-priced, meaning they represented more attractive bargains, while also benefiting from the fact that their lower prices enabled the portfolio to hold more shares, increasing the amount of dividends it would receive.3

Where one might think of the Dow as a collection of the "elite" corporations in America, the S&P 500 is more representative of the American corporate environment as a whole. Thus, where the PIC's focus on solid fundamentals might not mean much in the rarefied atmosphere of the Dow, it does select a "fundamentally" better group of companies from those available in the S&P 500.

The Dog strategy, on the other hand, in focusing on those companies having the highest dividend yield, has a greater chance of selecting companies that are failing or - at best - going through a period of "unfavorable" conditions. As with the Dogs of the Dow, the S&P Dogs, because of their lower value, were able to accumulate more shares of their holdings, resulting in more dividends. This would account for the fact that the Dogs, while significantly behind the PICs in performance, were able to make a close game of it in terms of total return.

Looking Ahead

I must admit to being a little disappointed that the PIC portfolios did not manage to beat either the Dow Jones or the S&P 500, and that I failed to beat the Dogs of the Dow is also something of a let-down. That said, however, both portfolios finished with performances of more than 20%, and the total return for the S&P PIC was more than 30% - ultimately, all fine finishes.

I see little to be gained by further comparison with the Dog strategy - I may be resigned to the fact that fundamentals do not guarantee a great investment, but then, neither does a high dividend yield. The two strategies are measuring different things with different assumptions at the root of each.

Moreover, there is some fine-tuning to be done to the PIC strategy. Thus far, I have been treating it like the Dog strategy - buy at the beginning of the year, and sell at the end of the year; this may not be the best approach for the PICs.

At the beginning of 3Q13 I "PIC-ed" a new portfolio for each index, and the results for the two "revised" PICs were interesting.

For the Dow, the only change in the portfolio was putting Walt Disney Co. (DIS) in the place of IBM (IBM). The result:

(click to enlarge)

Using whole shares only and limiting each holding to no more than $1,000.00, over the course of 26 weeks realized a performance of 9.38%; with dividends, the total return was 11.05%. In terms of performance alone, we can make this comparison: during the last half of this year, the original PIC portfolio only increased by 612 basis points - far less than the 938 basis points the mid-year replacement realized.4

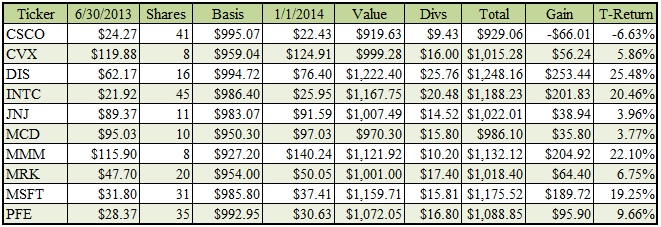

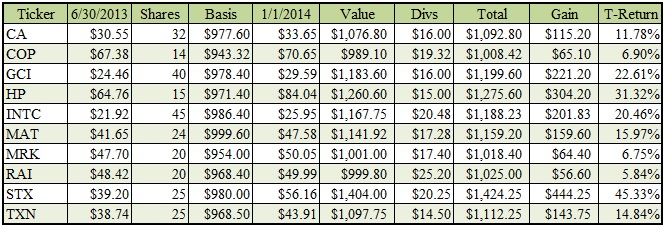

There were several changes to the S&P 500 PIC portfolio. The only original companies retained were Mattel, Inc. (MAT), Seagate Technology, Inc. PLC (STX), and Texas Instruments, Inc. (TXN). Added to the portfolio were CA Inc. (CA), ConocoPhillips (COP), Gannett Co., Inc. (GCI), Helmerich & Payne, Inc. (HP), Intel Corporation (INTC), Merck & Co., Inc. (MRK), and Reynolds American, Inc. (RAI). The following table shows the results:

(click to enlarge)

Again, the procedures of whole shares only, a limit of $1000.00 per company, were used. The results were quite dramatic: after six months, the portfolio increased in value by 16.39%, and with dividends added the total return was 18.26%. During this period the original PIC holdings increased in value by only 984 bps.

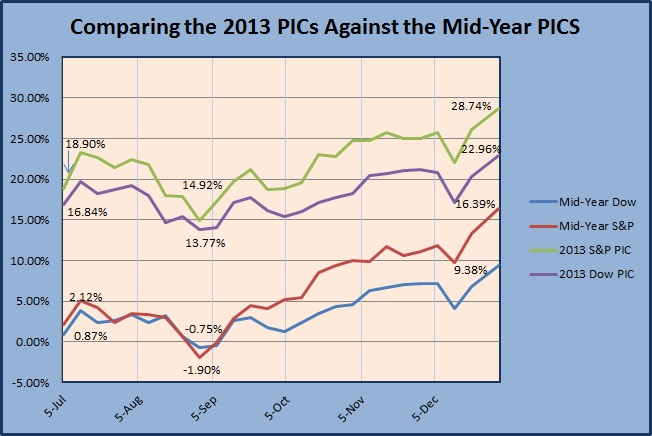

The following chart compares the performances of both the original PIC portfolios and the mid-year replacements:

(click to enlarge)

The two mid-year experiments have led me to wonder whether the PIC portfolio needs to be adjusted, and whether the adjustment needs to be made each quarter or whether a mid-year adjustment would suffice. The number of adjustments desirable is a question raised by the swoon that hit the markets for much of the month of August.5

I propose to continue the PIC study into 2014. The Dow and the S&P portfolios will start up where the 2013 portfolios ended, although the "whole share only" restriction will be put into place (since it is more realistic). A third portfolio will be added, chosen from all U.S. businesses.

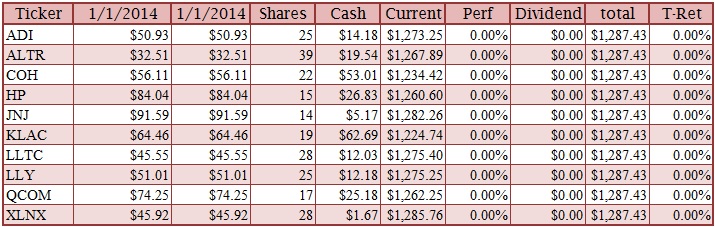

The 2014 Dow PIC

(click to enlarge)

The only change here is the addition of Nike, Inc. (NKE). The $12,648.90 earned by the 2013 portfolio has been split equally among the holdings. Excess is kept as a cash reserve.

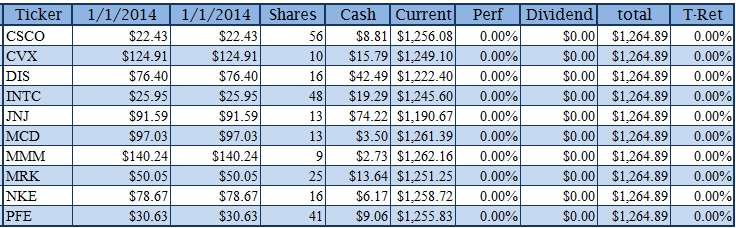

The 2014 S&P 500 PIC

(click to enlarge)

Analog Devices Inc. (ADI) returns to the list, as do Johnson & Johnson (JNJ), KLA-Tencor Corporation (KLAC), and Eli Lilly & Co. (LLY). New to the portfolio are: Altera Corp. (ALTR), Coach, Inc. (COH), Linear Technology Corp. (LLTC), Qualcomm, Inc. (QCOM), and Xilinx, Inc. (XLNX). Each company receives a share of 2013's earnings of $12,874.30.

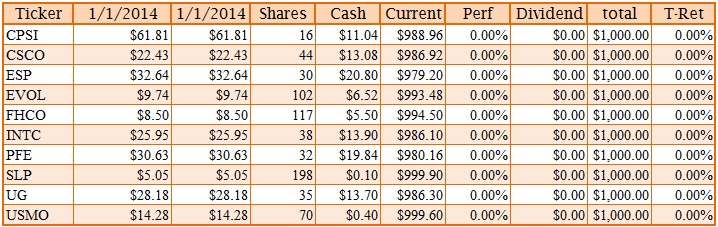

The "All-American" PIC

I had to ramp up the criteria to narrow down the candidates for this portfolio which is made up of ten companies, all headquartered in the U.S. The companies are:

- Computer Programs & Systems, Inc. (CPSI)

- Cisco Systems (CSCO)

- Espey Manufacturing & Electronics Corp. (ESP)

- Evolving Systems Inc. (EVOL)

- The Female Health Company (FHCO)

- Intel Corporation

- Pfizer, Inc. (PFE)

- Simulations Plus, Inc. (SLP)

- United-Guardian Inc. (UG)

- USA Mobility, Inc. (USMO)

As an index against which to compare the performance of this portfolio, I propose to use the New York Stock Exchange composite (the NYSE, although any readers who think a different index would be more appropriate are welcome to present their case in the comments, below). The companies will start with a $10,000.00 total basis, each company receiving $1,000.00, with the initial distribution as follows:

(click to enlarge)

Ultimately, each of the portfolios will have three versions: the original, to be carried through the entire year; a variant that will be adjusted quarterly; a variant that will only be adjusted at the beginning of 3Q14. I will keep interested parties posted on the portfolios' progress on my Instablog page - updates will be made monthly.

Disclaimers

This article is for informational use only. It is not intended as a recommendation or inducement to purchase or sell any financial instrument issued by or pertaining to any company or fund mentioned or described herein.

Before investing, readers are reminded that they are responsible for performing their own due diligence; they are also reminded that it is possible to lose part or all of their invested money.

All data contained herein is accurate to the best of my ability to ascertain. All opinions contained herein are mine unless otherwise indicated. The opinions of others that may be included are identified as such and do not necessarily reflect my own.

1 The three replacements, which were inconsequential to the Dogs strategy, were Goldman Sachs Group, Inc. (GS), Nike Incorporated (NKE) and Visa, Inc. (V).

2 It's not really clear that there was any consensus on what to do in this case, and even on one website you get two versions of the Dogs. One contains HP while the other contains Chevron.

3 The two portfolios had five holdings in common. Of the differing holdings, the PICs averaged 22.6 shares per company while the Dogs averaged 38.6 shares per company (figures approximate).

4 It should be noted that it was during the second half of the year that IBM had its meltdown, while Disney performed quite well.

5 It is also interesting to note that the mid-year replacement for the S&P PIC was hardly affected by the government shutdown, while the other three portfolios all show a marked decrease for that period.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire