Editors' Note: This article covers stocks trading with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

Apple's Fragile Pulse

Apple (AAPL) is a company that is very hard to knock. Many people I talk to see the company as all that America stands for in an entity -an American corporation that has out-innovated its peers through the genius of its genius leader. I am not here to knock Apple, although we are all here for one reason - to profit.

Once a company has grown into a mature state, an individual's return on investment will be nowhere near the same as it was during the company's high growth stage. The technology sector offers a funny retirement situation for technology companies. Either you mature into a Microsoft (MSFT) or IBM and offer consistent returns or dividends or you falter like BlackBerry (BBRY) or Hewlett-Packard (HPQ) before finding ground.

The point of the matter is not to exile all thoughts of Apple's products and to tell your kids to throw out their iPhones in favor of a new Galaxy (pun intended), but to put your hard-earned investment dollars into other companies that can offer a better return.

Lets Jump Into The Numbers:

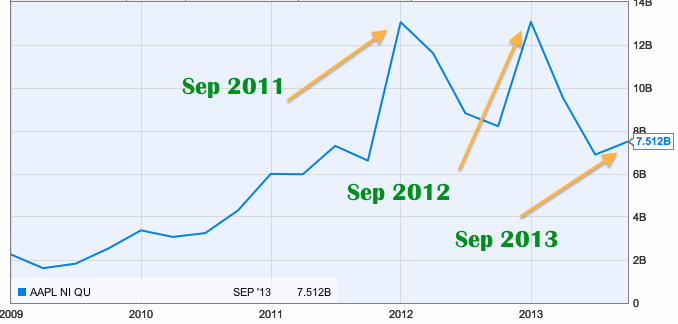

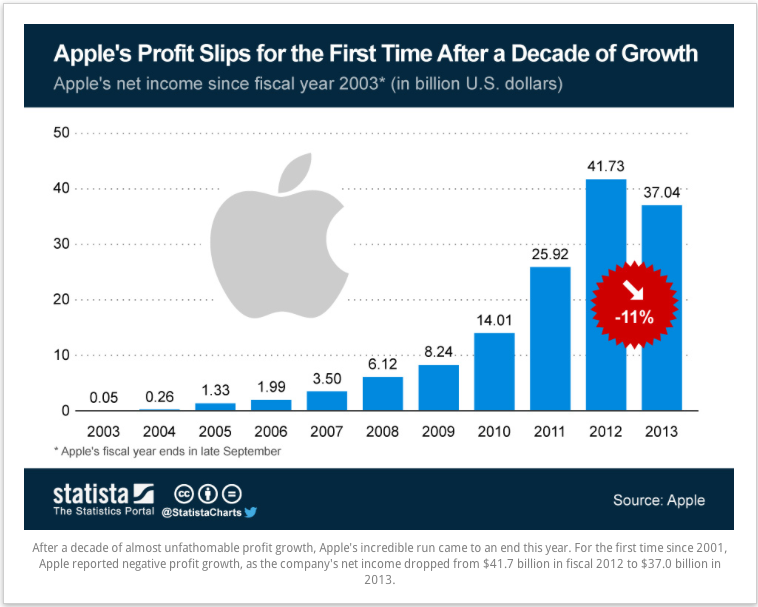

(click to enlarge)

It's no surprise that Apple's quarterly net income is falling. This year has been without the usual September spike in net income. That may change when this quarter is reported probably in late January due to holiday sales on the new iPad lineup and iPhone 5S. The iPad Air and iPad Mini with retina display and the iPhone 5S have all been huge hits.

Apple's slowing growth and future have not gone unbeknownst to the market - an excellent article on the short case can be read here for more information on the overall topic. Although the facts are clear, Apple's net income explosion cannot continue forever, so it has to slow down. Apple's pulse is still strong, but not as steadfast as it once was.

Jumping right into a DCF model I formulated on Apple, my calculations result in a slight 3.42% upside potential from current levels as of the writing of this article. This is based upon the assumption that Apple sees 9% growth over the first five years before tapering off to 7% and 5% for the second two five-year sets, respectively. I believe my estimates are in line with others who see low digit growth moving forward as well.

Apple is a $500 billion dollar company and as such 9% growth is a conservative estimate for a company who is facing stiff competition form Samsung (OTC:SSNLF) and the android world. As for my discount rate, I generally use 10%-12% for technology companies. I have chosen a middle ground to act as a conservative barrier for this analysis.

The Future Can Hold Twists:

Investing is far from black and white, it is extremely grey - to quote the awe-inspiring movie American Hustle in a form. There are many factors that can dictate a share price higher than what is calculated in this discussion.

Apple will likely see a news driven bump when it reports earnings in January driven by holiday sales of its wide new product lineups. The problem is that Apple's earnings power is becoming limited to select quarters, not an overall annual basis.

With regard to advancements, Apple is the same to innovation as Albert Einstein to gravity. The company will likely release an iTV that will blow consumers away. Furthermore, the company's iWatch will likely be a huge hit that will look even better in comparison to Samsung's smart watch launch. These new products will increase Apple's brand power moat and in turn, the company's ecosystem.

Samsung's devices are also without the Apple ecosystem that many enjoy. I have written extensively on VirnetX (VHC), and in researching the company I have grown aware to the secure features surrounding iMessage and FaceTime. As I have stated, I love Apple's products.

The Samsung Problem:

Other than the fact that Samsung leads the way on 4G LTE-Advanced capabilities in its newer smartphones, the new age of wireless speeds, Samsung has many growing advantages. One of these items is that Samsung can offer better specifications on its phones than Apple for the same price. An example is the equal $299 price for an iPhone 5S and Galaxy note III on contract. The note offers 1.7" more screen size on a higher resolution display, 2 extra gigs of ram and the 4G LTE-A capable Snapdragon 800 chip.

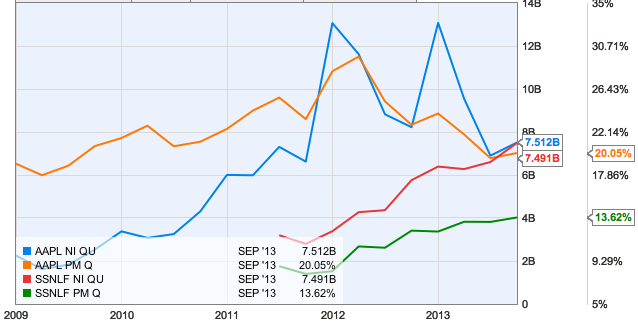

(click to enlarge)

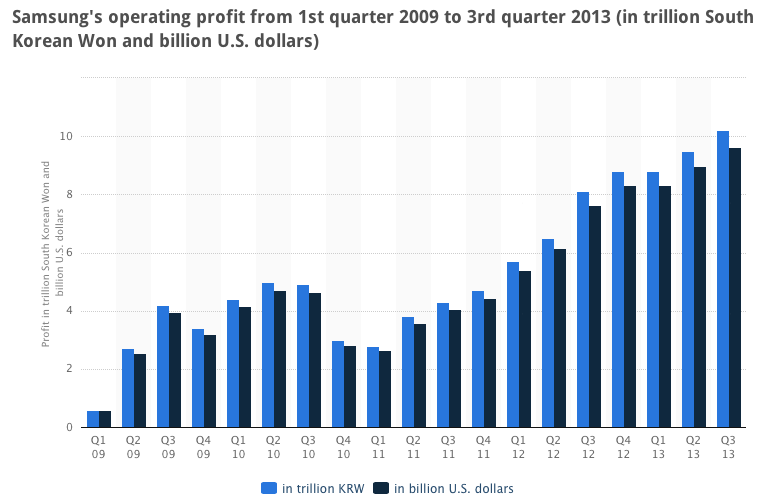

The chart above can be difficult to read on first glance. To make things easier, Apple's quarterly net income is shown in blue and quarterly profit margin is in orange. While Samsung's are in red and green respectively. The trend above shows an interesting development - Apple's net income and profit margin is falling while both of Samsung's are rising.

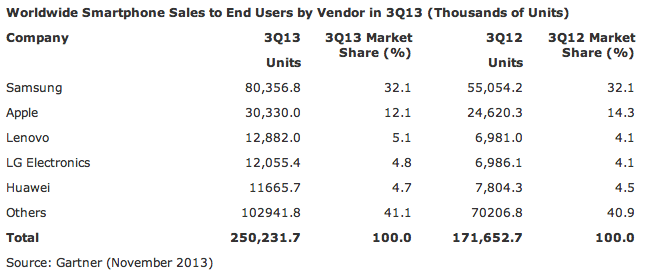

(click to enlarge)

It is not that Apple has maxed out its smartphone market share; they are only at 12% reported by Gartner. The iPhone is the most important driver of Apple's earnings. The problem is that Samsung is leading in smartphone market share. And as such, Samsung does not need to eradicate Apple's 12% share, they just have to keep growing at the loss of other companies like Lenovo and LG. Samsung's net income has been on the rise due to the company's ability to do this successfully and profit from it.

Now you tell me who makes more money as a company - Honda selling their cars to the mass population or Ferrari selling their vehicles to the elite. The difference in these cars is much greater than the difference in a Galaxy S4 to an iPhone 5S as well.

The China Mobile Deal:

The China Mobile deal was talked about incessantly as the next driver for Apple's continued smartphone domination. Estimates have been thrown around as to the amount of iPhone sales, although 34-35 million is the consensus estimate. There is no doubt that this could add $4 to $5 in EPS to Apple's earnings moving forward.

This is what I also attribute to the large holiday sales of Apple's new products that will likely drive the coming quarter's earnings. This will boost shareholder morale, and in turn the share price. Although think afterwards, think long term, thing of a maturing company at a new stage. If you think Apple is facing stiff competition her in America, just think of the competition abroad where Samsung does a large percentage of its business. Keep in mind that China Mobile (CHL) already has north of 42 million iPhone users already.

The Trend:

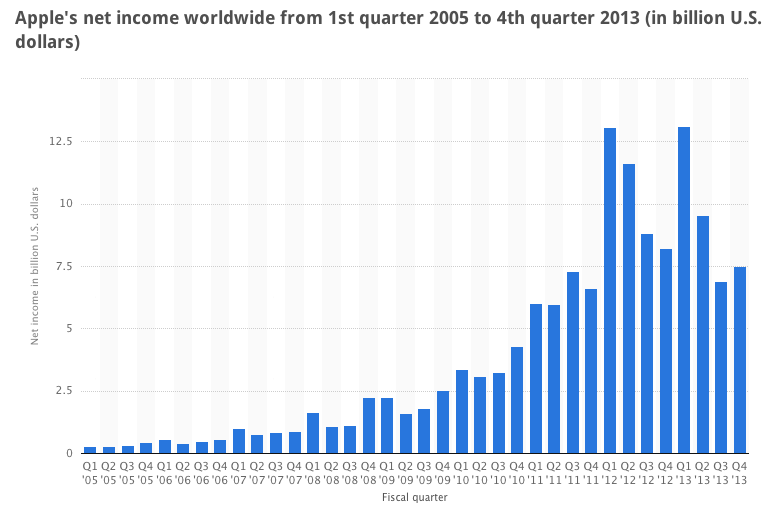

(click to enlarge)

Apple is starting to transition into a mature technology company. As such net income is starting to taper off from the ultra high levels that have been seen in the past.

(click to enlarge)

This notion can be seen first in 2013 as Apple's profit slipped after a decade of growth. Will Apple have a rebound quarter? I am very confidant that Apple will blow out this quarter's earnings on the back of holiday sales for its new iPhone 5S and new iPad lineup coupled with the China Mobile Deal. As such I would not recommend taking a short position until after any spike, when everything is wonderful.

(click to enlarge)

With over 1 billion Android activations, the other side of the smart phone playing field is not slowing down. Samsung has also been highly successful in capturing the growth of Android in recent time, and that has grown Samsung's profit tremendously.

(click to enlarge)

Technology Investing Alternatives:

As I said, I am not here to bash Apple - just to distinguish between investments to earn the most ROI for my investing dollars. One such idea that could yield impressive returns for investors is SuperCom (SPCB). The company recently acquired OTI's Smart ID division that is extremely accretive to the company. My analysis puts the technology company at $6 to $8, and Lazarus Investment Partner's excellent article disseminates their bullish view on SuperCom as well. From the $4.60 range, this would amount a gain in the area of 30% to 74% if all pans out well

Another technology alternative that I wrote about earlier this month is NetSol Technologies (NTWK). The company has been on the decline, although their recent operational result demonstrates serious improvement. The limbo sales period in-between the company's launch of its new legacy product also offers a decrease share price that investors can take advantage of right now, prior to full-fledged sales. Stanley Barton provided an in-depth analysis recently on the company as well that can be viewed here.

Conclusion:

The problem is long term, not short term. Apple has a brand power that many optimists even discount. No one talks about any future Samsung or Android operating system updates - although they are starting to. Consumers are beginning to realize that other companies can offer products with better or comparable specifications at the same or a cheaper price. Apple's brand-power is its most powerful asset in my opinion; any erosion of this should have investors looking for investment alternatives.

Just a few months ago, I was deciding whether or not to buy an iPhone 5S or a Samsung Galaxy S4. Having had numerous phones from a wide array of brands, I am not new to the game. The interesting part was how undecided I was. I decided on the iPhone 5S due to its awesome graphics power that I previously wrote about, although the debate has grown closer.

Apple is transitioning into a mature company. Samsung is still in the high growth phase as its income is ballooning as sales expand. In my opinion I love Apple's products, although the opportunity cost of investing in Apple is becoming too great in the face of compelling alternatives. I would like to reiterate my view that Apple will likely blowout earnings on the back of its new products and the China Mobile deal, so be aware. If Apple's pulse is growing weaker, move your investing dollars into a better investment vehicle that offers the greatest BPM (best practical means) for your investing dollars.

Best to all investors and enjoy your New Year

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

Additional disclosure: Always do your own research and contact a financial professional before executing any trades. This article is informational and in my own personal opinion.

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire