As a fascinated spectator of the Fed's often unpredictable monetary policy, it has become clear that few, if any, market experts understand the implications of Quantitative Easing (QE). That is not a criticism, but a stark observation.

Larry Summers created quite a ruckus in early November when he re-introduced the term "secular stagnation" during an IMF forum. His theory--in short, that real interest rates dipped below the zero bound--is indeed mind boggling, if only because it runs counter to modern economic policy and suggests a market economy so contrarian to current conditions. Such economists as Paul Krugman have rallied behind the idea. The lesson I wish to take from Summers' hypothesis is that relational thinking is key to financial literacy. Summers figures that with the velocity of M2 at an all time low and the latest credit bubble creating little excess in aggregate demand, previously unconsidered phenomena are emerging.

In this article, I wish to, briefly, focus on one such phenomenon: the net interest rate margin (NIRM). This statistic can contribute to a larger narrative about the future and profitability of America's biggest banks.

2014: Escaping the Profit Squeeze

Since lowering its interest rate in 2008, the Fed has effectively eliminated the cost of capital for banks. From the end of 2008 through the third quarter of this year, U.S. banks have reported nearly $214 billion in profits, in no small part because of the Fed's easy money policy. Yet the Fed's commitment to low rates is a mixed bag: though it reduces borrowing costs, it also places a damper on how much banks can charge for outgoing loans and other investments.

The graph below shows the net interest rate margin for U.S. banks since 1980.

(click to enlarge) Source: FRED

Source: FRED

The NIRM accounts for the difference between a firm's borrowing costs and lending rates. This difference has been steadily declining since QE began in earnest in 2010. Traditionally, the spread a given bank can make from loans is positively correlated with interest rates, thus allowing a firm to pad profits onto its bottom line as liquidity becomes more expensive.

Yet NIRM must be contextualized. Higher rates may only improve the profitability of banks if (1) they don't lead to a corresponding decrease in consumer loan demand and (2) they don't affect a bank's underlying position through hefty paper losses. Fatter spreads mean nothing if not accompanied by a strong economy, and the long-term outlook for U.S. GDP growth does not look promising. Moreover, even the current low-interest environment has produced staggering excess reserves. This excess may be attributed to either a lack of demand or some clever craft work by banks, who earn a healthy 0.25% with the Fed or can choose to re-invest their free money in Treasuries. From 2007 to 2013, excess reserves skyrocketed.

(click to enlarge)

Source: FRED

This excess in reserves may be a sign that private sector and consumer lending remain stagnant. Furthermore, "traditional" banking, in which banks lend out depositor funds and capitalize on returns, is no longer the bread and butter of most financial institutions. In fact, because households have been deleveraging since 2008, demand for loans has been anemic, causing banks to re-focus on their capital market divisions: stock offerings, M&As, and other specialized forms of asset allocation. A rising interest rate environment, then, may not be the primrose path for the Fed.

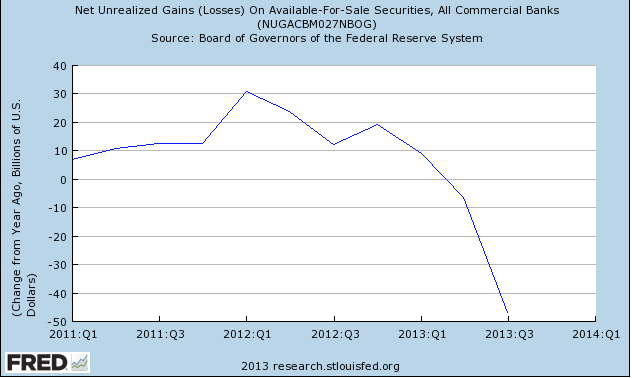

Moreover, banks have endured hefty paper losses this year due to gains in Treasury yields.

(click to enlarge)

Source: FRED

Treasury yields have led to a massive sell-off in the corporate bond markets, forcing banks to stomach huge losses. These losses are important on several levels. First, they shave the value of security holdings and prevent banks from finding more efficient ways to meet minimal capital requirements. In June, Bank of America's CFO conceded that recovering a decline in capital through extra interest income could take 2 to 3 years. Even a 50 basis point increase in Treasuries could have massive repercussions for corporate balance sheets, limiting the flexibility of loan portfolios and pressuring banks to squeeze money out of other divisions.

Conclusion

The net interest margin remains an important benchmark for banks. In the long-run, investors and banks will benefit from higher interest rates that spur attractive spreads.

Investors must, however, be wary of NIRM's shortcomings, namely that consumer and private sector loan demand must pick up before banks can take full advantage of rising interest rates. And balance sheet reduction through heavy capital losses may cut into the potential upside provided by increased yields.

These realities may be good news for investors, who, as interest rates inevitably rise, will once again become valuable customers and seek out institutions offering attractive deposit rates, perhaps setting in motion a consumer-driven price war. As banks like Bank of America (BAC), which sold its non-U.S. private banking operations last year, whittle down unprofitable holdings and devote their energies towards regulation-friendly divisions, investors can expect higher dividends and more share buy-backs, both of which will buttress market sentiment and release excess capital. The KBW Bank Index was up 20 percent in the first half of 2013 on taper expectations, a trend sure to continue once Janet Yellen takes the helm at the Fed.

As banks continue to find their post-crisis identity somewhere in the spectrum of lenders to traders, interest rates will persist as a double-edged sword. Prudent investors would do well to keep a close eye on how net interest rate margins react to restructured banks and the Fed's fickle monetary policy. If it's any indication, about 40% of Berkshire Hathaway's (BRK.A) (BRK.B) current equity portfolio is concentrated in the financial services industry, suggesting that at least one investor believes that higher interest rates will be more of a blessing than a curse.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire